Impact of the COVID-19 Pandemic on Multi-airport Systems Worldwide

Xiangru Wu[1], Xiaowen Fu[1], Zheng Lei[2] and Kun Wang[1] [1]Department of Industrial and Systems Engineering, The Hong Kong Polytechnic University, Hong Kong, China [2]Department of Aviation, Swinburne University of Technology, Australia

Abstract: This study examines the impacts of the COVID-19 pandemic on

multi-airport systems (MASs) worldwide. First, the recent literature on

MASs is reviewed to identify emerging research topics and development

patterns. Then, airline schedule data are collected for 53 sample MASs

and used to analyse three dimensions of MAS structures before and during

the late stage of the pandemic: (i) traffic and degree centrality

distribution within MASs, (ii) intra-MAS airport competition; and (iii)

airline competition intensity within MASs. The empirical findings reveal

that MAS structures in Europe and the US have remained relatively stable

despite the recent pandemic, partly because compared with Asia Pacific,

air travel bans in these markets were lifted earlier, and domestic and

international airline markets have largely returned to pre-pandemic

levels. In comparison, significant changes have been observed in

Asia-Pacific MASs due to restrictive bans on international travel and

airline operations. As major airlines shifted capacity to domestic

markets, in Asia Pacific intra-MAS airport traffic distribution became

more balanced, intra-MAS airport competition intensified, smaller

airlines dropped out, and airline concentration levels increased. In

addition, with more under-utilized slots available, Chinese low-cost

carriers increasingly consolidated their operations to selected airports

within MASs which would allow them to achieve economies of scale.

Overall, this study provides insights into the adaptability of MAS

structures in the face of a global crisis.

Keywords:Multi-airport system (MAS);COVID-19 pandemic;Full-service carrier (FSC);Low-cost carrier (LCC) Citation:Wu, X., Fu, X., Lei, Z., and Wang, K. (2023). Impact of the COVID-19 Pandemic on Multi-airport Systems Worldwide. Journal of the Air Transport Research Society 1(1): 117-135 DOI:https://dx.doi.org/10.59521/225FA3D62802E847 Download:PDF

1 Introduction

The air transport industrys rapid growth in recent decades has led to

the fast development of multi-airport systems (MASs) around the world.

In addition to well-known systems in London, New York, Tokyo, and Paris,

emerging countries with booming airline markets, particularly China,

have also developed MASs (Hou et al., 2022). MASs not only alleviate

airport capacity constraints but also optimize airline services and

connectivity for metropolitan areas. Some MASs have airports serving

distinct market positions to diversify the airline services in one

metropolitan area. At the same time, the inter-airport competition

within MASs can reduce airfares and increase flight frequencies,

benefiting passengers and regional economies (Winston and Yan, 2011). A

well-functioning MAS thus stimulates air traffic and coordinates

economic development within and across regions (Brueckner, 2003; Sheard,

2014). The strategic interactions among airports and airlines are more

complex in the presence of MASs, involving decisions about flight

frequency, airfares, airport entries, and network development.

Passengers airport choices depend on factors such as ground access,

flight networks, schedules, and airfares. Previous studies have

documented these issues through theoretical and empirical approaches, as

summarized and discussed in Section 2 of

this paper.

The COVID-19 pandemic (hereafter referred to as “the pandemic”) has

had unprecedented impacts on the entire airline industry, and extensive

research has been conducted to understand its effects from different

perspectives (Sun et al., 2020; Nižetić, 2020; Suzumura et al., 2020;

Zhang et al.,2021; Czerny et al. 2021). Existing studies of the

pandemic’s impact on airport operations have mainly focused on

individual airports of different sizes and regions. Travel restrictions

have severely damaged international connectivity for major regional

gateway airports worldwide, while domestic aviation markets have

generally recovered as outbreaks have been contained domestically,

despite several waves of local outbreaks. The pandemics impact on

airports may also depend on their network structure, such as

hub-and-spoke vs. point-to-point, as well as the type of airlines

(full-service carriers (FSCs) vs. low-cost carriers (LCCs)) and airline

dominance at a particular airport, because such factors are likely to

moderate the pandemics effect on airport operations, airline competition

and dominance, and network configuration (Fu et al. 2015a, 2019).

Despite extensive research on the impacts of the pandemic on the air

transport industry, there has been relatively little investigation into

how MASs have been affected. Many questions remain unanswered in this

area. First, the pandemic could have affected different airports in the

same MAS differently, causing changes in traffic and connectivity

distributions among individual airports. Second, inter-airport

competition within MASs might have been affected, with market coverage

converging (serving more common destinations) or diverging (serving

fewer common destinations) during the pandemic. Last, the pandemic could

have caused variations in airline competition (including that among

airlines providing differentiated services, such as FSCs vs. LCCs (Fu et

al. 2011)) and their dominance among different airports (such as an

airports hub status). For example, Londons metropolitan area is served

by six international airports, with Heathrow (LHR) dominated by British

Airways and Gatwick (LGW) as a main base for Easyjet, a low-cost

carrier. The pandemic is likely to have imposed heterogeneous impacts on

these airports within the London MAS, which could have significant

implications on airline competition, airport capacity/slot use, and

airport connectivity. The pattern and magnitudes of such impacts

nevertheless remain unclear to industry and policy makers. This study

aims to address these gaps in the literature by examining the impacts of

the pandemic on MASs worldwide, shedding light on the changes and

development patterns of these systems.

To address the research questions outlined above, we collected

airline scheduled seat data for 53 MASs worldwide over the 2018-2022

period. Several statistics and indices were calculated and benchmarked

before and during the late stage of the pandemic, with a focus on the

relatively long-term impact of the pandemic. We conducted an intra-MAS

analysis to examine the heterogeneous impacts of the pandemic on the

traffic and network size of airports within the same MAS, calculating

the Gini index of scheduled capacity and the degree of centrality for

each MAS. Additionally, we constructed a Herfindahl-Hirschman Index

(HHI) using the capacity share of flights with the same destination but

originating from different airports within an MAS, to measure the level

of intra-MAS airport competition. We were also interested in checking

the change in this index during the pandemic. To examine inter-airline

competition, particularly between FSCs and LCCs within an MAS, we

calculated and compared the Gini index of the airlines market shares in

each MAS before and during the late stage of the pandemic. We conducted

these analyses for each sample MAS and conducted cross-regional

comparisons to shed light on heterogeneous patterns among different

regions worldwide, including the US, Europe, and the Asia-Pacific.

The remainder of this paper is structured as follows. Section 2 provides a review of the

relevant literature on MAS published in recent years, revealing recent

MAS developments and relevant research hotspots worldwide. Section 3 describes the data used in this

research, including the definition and selection of sample MASs for this

study. In Section 4, we conduct a series of

calculations based on the statistics and indices described in the

previous paragraph and provide a discussion and interpretation of the

results. Finally, Section 5

provides concluding remarks for this study.

2 Literature Review

This section presents a review and summary of the recent literature

on MAS development, with a focus on academic publications in the past

decade (since 2013) related to MAS management and economic issues.

Relevant studies can be broadly categorized into two categories: those

investigating passengers airport choices within an MAS and those

examining airline/airport competition within an MAS. Additionally, we

review recent studies of the impacts of the pandemic on airport

operations, which should provide useful insights into the impacts on

MASs.

2.1 Passengers’ airport choices in

MASs

Since the 1980s, it has been a common research strategy to examine

passengers airport choices within an MAS. Analytical and empirical

research has explored the factors influencing passengers airport

choices, with a focus on some major MASs in the US and Europe,

particularly San Francisco, New York, and London (Harvey, 1987; Pels et

al., 2000, 2001, 2003; Hess et al., 2006; Marcucci and Gatta, 2011,

2012; Murça et al., 2013). These studies suggest that the ground access

time and cost, flight frequency, and flight time play important roles in

determining passengers airport choices, with passengers

exhibiting heterogeneous preferences for different factors.

In recent years, an increasing number of researchers have paid

attention to MASs in developing countries, such as China, Iran,

Slovenia, and Brazil. Table 1 summarizes papers on this topic published

in the last decade, which focused on different factors that shape

passengers airport choices. In addition to the

aforementioned influencing factors, recent studies have also considered

new factors related to passengers perceptions of service quality, such

as safety and punctuality, which also contribute significantly to

passengers choice decisions. Some studies investigate air-rail

intermodal transport for MAS connectivity and its influence on

passengers airport choices. Both theoretical and empirical studies have

suggested that passengers choose air-rail intermodal transport if one

airport has better integration with high-speed rail (HSR) service, such

as Hongqiao Airport in Shanghai MAS and Daxing Airport in Beijing MAS,

due to considerations related to the contingency arrangement in case of

delays and regarding checking-in, comfort, and luggage

deposits (Chiambaretto et al., 2013; Li et al., 2020; Wang et al., 2020a;

Babić et al., 2022).

Table 1: Recent literature on passenger airport choice in MAS

Author/Year

Studied MAS

Model

Specifications/Findings

Fuellhart et al. (2013)

Boston, Washington, and San Francisco, the

US

Higher route-level airfares and longer

route distance lead to an apparent switching of passengers’ airport

choices. This means passengers may be willing to make changes to a

preferred airport for longer distance trips.

Mamdoohi et al. (2014)

Tehran MAS, Iran

Binary Logit model; Focus on the

difference of airport choice between resident and non-resident and find

that public access, flight frequency, and airport tax are more important

for non-resident air travelers when choose their origin airport.

Paliska et al. (2016)

Upper Adriatic region, Slovenia

Mixed logit model; Access time to airport

is the most important determinant in airport choice for all kinds

travelers (business/leisure and cross-border/domestic) and borders have

an influence on airport choice.

Jung and Yoo (2016)

Seoul MAS, South Korea

Two-level Nested Logit model; The results

show that fare, flight time, frequency, access time, access cost and

airport access convenience latent variables are significantly affecting

passengers airport choice behavior.

Bezerra and Gomes, (2019)

São Paulo MAS, Brazil

Partial least squares–structural equation

model; Support airport service quality as a determinant of passenger

loyalty. Marketing and operational strategies based on customer

segmentation help to strengthen the passenger loyalty to the

airport.

Tiglao (2020)

Aklan MAS, Philippines

Discrete choice model; Tourist passenger

do put high premium in air safety.

Teixeira and Derudder (2021)

New York MAS, the US

Huff models; Consider the spatio-temporal

dynamics in airport catchment areas and calculate airport attractiveness

to passengers in different census block groups.

Liao et al. (2022)

Guangdong-Hong Kong-Macao Greater Bay Area

(GBA), China

Partial least squares structural equation

model; Confirm positive relationships between airport service quality

and passengers’ intention to reuse an airport.

2.2 Airline or airport competition

in MASs

As mentioned in the introduction, the presence of an MAS enhances

strategic interactions among airports in a region and intensifies both

inter- and intra-airport airline competition. In recent years,

researchers have paid increasing attention to the privatization of one

or more airports within an MAS, following the global trend towards

airport corporatization. This trend has been particularly notable in

China, where several airports have consolidated to form airport group

companies to improve profitability and achieve better coordination.

Furthermore, the prevalence of HSR has significantly reshaped the

intercity transport market, particularly in China. The integration of

air and HSR transport with some airports within an MAS can significantly

affect airport and airline competition and coordination behaviour.

Recent studies have investigated the impacts of these developments on

MASs and their implications for airport and airline operations and

competition. Table 2 provides a summary of these studies published over

the past decade.

Table 2: Recent literature on inter-airport and airline competition in

MAS

Author/Year

Studied MAS

Model

Specifications/Findings

Yan and Winston (2014)

San Francisco Bay area, the US

Focus on the private airport competition

and find that private airport competition could increase commercial

travelers welfare and airlines profits and enable the airports to be

profitable.

Liao et al. (2019)

Guangdong-Hong Kong-Macao Greater Bay Area

(GBA), China

Three liner models; Focus on the route

level competition between airports in GBA-MAS and its impact on

passenger airport choice.

Wong et al. (2019a)

MAC around world

With the competition of FSCs, LCC shift

focus from smaller airports in MAR to non-MAR airports.

Wong et al. (2019b)

MAC around world

Discuss the competition for passengers

among hubs and secondary airports in multi-airport cities.

Cheung et al. (2020)

Guangdong-Hong Kong-Macao Great Bay Area

MAS, China

Dynamic spatial panel regression model,

the model provides a new tool in airport competition study. This paper

focus on the spatial interactions and spillover effects in the presence

of airport competition.

Hou et al. (2022)

Beijing MAS, China

Multi-stage game-theoretical model; Focus

on the impact of government intervention on airport competition. Find

that without government intervention in airline allocation between the

two airports, airlines would always prefer to enter both airports in the

MAS, leading to both an inter-airport and an intra-airport competition

structure.

de Paula Balan et al. (2022)

São Paulo and Rio de Janeiro MAS,

Brazil

Increased overlap routes in MASs were

healthy for competition between airports and airlines over the

years.

Li et al. (2022)

Theoretical analysis

Investigates the effects of air and

high-speed rail (HSR) cooperation on airport competition in MAS and

social welfare.

2.3 The impact of the pandemic on

the airport

The pandemic has had an unprecedented impact on the aviation

industry, as evidenced by recent studies (Zhang et al., 2020; Sun et

al., 2020; Czerny et al., 2021; Sun et al., 2021a; Salesi et al., 2022).

Researchers have conducted numerous investigations into the pandemics

effects on airport connectivity and operations and its heterogeneous

impacts across different airports and regions. Sun et al. (2022)

provided a comprehensive review of the research on the pandemic and air

transport. Specifically, regarding the impact on airport operations,

many studies have focused on the passenger travel experience during the

pandemic. For example, Li et al. (2022) used a data-driven

crowd-sourcing approach to study airport service quality during the

pandemic. Ma et al. (2022) built a structural equation model to

investigate the influences of four attributes of the airport physical

environment on passengers perceived safety, satisfaction, and travel

intentions during the pandemic. Zhang et al. (2021) used passengers air

ticket booking transaction data and airport arrival data to empirically

examine passengers travel behaviours during the pandemic and found that

passengers arrived at the airport earlier to undergo health check

procedures, despite having fewer opportunities to shop and dine at

airports. Chen (2022a, b) also found very obvious empirical evidence for

the substitutability of online meetings for air travel among

heterogeneous traveller, which could also cause changes in passenger

composition and air travel behaviour during and after the pandemic.

Many researchers have focused on the impact of the pandemic on

airport connectivity and have found that airport networks changed

significantly during the pandemic. These changes include shifts in

airport degree centrality, international connections, and network

connectivity (Sun et al., 2020, 2021b; Li et al., 2021; Kuo et al.,

2022). Several studies have concluded that the pandemic has had a

greater impact on international flights than on domestic flights, and

that the recovery speed of local connectivity has been faster than that

of global connectivity (Sun et al., 2020, 2021b; Li et al., 2021; Zhang

et al., 2022). For example, researchers studying Incheon International

Airport discovered that although the airports efficiency decreased

during the pandemic, the increase in connectivity between Incheon and

other airports could improve the airports efficiency (Shamohammadi et

al., 2022).

Some studies have shed light on the heterogeneous impact of the

pandemic on different types of airports, including hub and nonhub

airports. For example, Mueller (2022) found that non-hub airports in

Europe experienced more negative impacts than hub airports. Airports

primarily served by LCCs were more likely to be cut off from the network

during extensive network shrinkage than those served by FSCs. Other

studies have examined the heterogeneous impacts of the pandemic across

different regions and countries. Sun et al. (2020) reported that Europe

has undergone more significant changes in network connectivity than

North America. Many countries in North America, such as the United

States, Canada, and Mexico, remained highly connected with other

countries during the pandemic. Sun et al. (2021b) also found that,

compared to other countries, the impact of the pandemic on airports in

the United States was relatively homogeneous, with most airports only

partially affected. Although there have been many studies that have

explored the impacts of the pandemic on airports from different aspects,

there are still no papers dedicated to examining the impact on MASs. For

the characteristics of MASs, this study aims to investigate this topic

to fill this research gap.

3 Data and MAS Samples

An MAS is defined as a set of two or more commercial airports that

serve air traffic within a metropolitan region (Bonnefoy et al., 2010),

regardless of the ownership or political control of individual airports

(de Neufville, 2004). In this paper, we adopt the

definition of Bonnefoy et al. (2010) to select sample MASs. Bonnefoy et

al. (2010) used worldwide airport passenger traffic data from the

International Civil Aviation Organization (ICAO) (2008) and the Federal

Aviation Administration (2007), including all airports with more than

500,000 passengers in 2005. A geographical cluster analysis was

conducted to identify MASs. To identify all airports located within a

60-mile radius of the city centre, clusters of two or more significant

airports within 120 miles of each other were first identified. Then,

certain MASs were excluded based on geographical characteristics, such

as the presence of islands and the criterion that the largest airport

served fewer than two million passengers per year. Based on this

analysis, they identified 59 MASs, which was updated to 60 in 2011 (de

Neufville, 2016). Sun et al. (2017) also defined major commercial

airports as those with at least two million passengers per year.

We retrieved our airline scheduled seat data from the Official

Airline Guide (OAG) for the sampled MASs as identified in Bonnefoy et

al. (2010). These data include departure and arrival airports and

airline-specific scheduled seats on a quarterly basis for the 149

airports in the 60 sample MASs from Q1 2018 to Q4 2022, covering both

the pre-pandemic and the pandemic periods. The OAG database also

includes variables indicating whether a route is domestic or

international, and whether an operating airline is an FSC or an LCC.

However, during our study period, one airport in each of the Belo

Horizonte, Gothenburg, Tel Aviv, and Berlin MASs closed, leading us to

exclude these four systems. Additionally, Beijing was included in the

MAS list by Bonnefoy (2010), since the city is served by two airports.

However, Nanyuan Airport serves only regional routes out of Beijing

under special approval granted to selected airlines only and is much

smaller than Beijing Capital Airport. Therefore, we also excluded

Beijing from our sample.1 Similarly, Lübeck Airport in the

Hamburg MAS only serves a limited number of regional routes, leading us

to exclude Hamburg as well. In the end, we identified a total of 53 MAS

in 24 countries for study, as shown in Table 3.

Table 3: Sample MASs in this study

Region

MAS Country

Airports

MAS Country

Airports

Asia-Pacific

Melbourne AU

Melbourne, Avalon

Hong Kong CN

Hong Kong, Shenzhen

Shanghai CN

Pudong, Hongqiao

Taipei CN

Taoyuan, Songshan

Osaka JP

Kansai, Itami, Kobe

Tokyo JP

Haneda, Narita

Seoul KR

Incheon, Gimpo

Bangkok TH

Suvarnabhumi, Don Mueang

Europe

Brussels BE

Brussels, S. Charleroi, Liege

Paris FR

de Gaulle, Orly, Beauvais-Tille,

Chalons-Vatry,

Dusseldorf DE

Duesseldorf, Cologne-Bonn, Dortmund,

Weeze

Frankfurt DE

Frankfurt, Hahn

Stuttgart DE

Stuttgart, Baden

Milan IT

Malpensa, Bergamo, Linate

Pisa IT

Pisa, Florence

Rome IT

Fiumicino, Ciampino

Venice IT

Marco Polo, Treviso

Amsterdam NL

Amsterdam, Eindhoven, Rotterdam

Oslo NO

Gardermoen, Sandefjord-Torp

Moscow RU

Sheremetyevo, Domodedovo, Vnukovo

Vienna SK

Vienna, Bratislava

Barcelona ES

Barcelona, Girona, Reus

Copenhagen SE

Copenhagen, Malmo

Stockholm SE

Arlanda, Bromma, Skavsta

Istanbul TR

Istanbul, Sabiha Gokcen

Belfast UK

Belfast, George Best

Glasgow UK

Edinburgh, Glasgow, Prestwick

London UK

Heathrow, Gatwick, Stansted, Luton, London

City

Manchester UK

Manchester, Liverpool, Leeds Bradford

Latin America & Middle East

Buenos AR

Newbery, Ministro Pistarini

Rio de Janeiro BR

Rio de Janeiro, Santos Dumont

Sao Paulo BR

Guarulhos, Congonhas, Campinas

Tehran IR

Mehrabad, Khomeini

Mexico City MX

Mexico City, Toluca

Dubai AE

Dubai, Sharjah

North America

Toronto CA

Pearson, Billy Bishop, Hamilton

Vancouver CA

Vancouver, Abbotsford

San Diego US

San Diego, Tijuana

Boston US

Logan, Providence, Manchester-Boston

Chicago US

OHare, Midway, Rockford

Cleveland US

Hopkins, Akron

Dallas US

Dallas, Love Field

Detroit US

Metropolitan Wayne, Flint

Houston US

George Bush, Hobby

Los Angeles US

Los Angeles, Santa Ana, Burbank, Ontario,

Long Beach

Miami US

Miami, Lauderdale

New York US

Kennedy, Liberty, LaGuardia, Islip

Norfolk US

Norfolk, Williamsburg

Orlando US

Orlando, Sanford

Philadelphia US

Philadelphia, Atlantic City

San Francisco US

San Francisco, San Jose, Oakland

Tampa US

Tampa, St Pete-Clearwater, Sarasota

Washington US

Baltimore, Dulles, Reagan

4 Statistics and Discussions

In this section, we calculate and discuss some statistics and indices

to shed light on the impact of the pandemic on MASs worldwide. For

concise discussions and clear insights, we concentrate on the major MASs

in each region (i.e., North America, Europe and Asia Pacific) while

reporting the statistics of all sample MASs in the appendix.

4.1 Traffic and network size

distribution within MAS

Individual airports within an MAS may focus on different markets or

be served by different types of airlines. For example, FSCs may utilize

hub airports to develop extensive regional and inter-continental

networks that enable them to leverage various cost and competitive

advantages (Zhang 1996; Tu et al, 2020), whereas secondary airports may

focus on regional destinations and serve many LCC flights (Wang et al.

2020b). Airlines’ frequency choices depend significantly on traffic

volume and slot availability, which in term further affect service

equality and passenger demand (Wang et al. 2014). The pandemic cause

significant yet non-uniform demand reduction, which are likely to have

imposed heterogeneous impacts on different airports. To capture the

degree of possible uneven or unequal distributions among various

entities, we adopt the Gini index as a commonly used measure. We

calculate the Gini index of traffic and degree centrality for the

sampled MASs before and during the late stage of the pandemic, based on

data from Q3 2019 and 2022. The degree centrality is defined as the

total number of destinations linked with each airport via direct

flights, and it helps to measure the network scope of a particular

airport. The Gini index is calculated using the following equation,

which measures the degree of inequality in the distribution of airport

traffic within the same MAS: GM=( \textstyle åi=1m

\textstyle åj=1m

| Yit-Yjt

| )/(2m2Ym ), where Yi is the degree

centrality or scheduled seats of airport i, and m is the number of airports in one

MAS. The Gini coefficient is GM and it can

theoretically range from 0 (complete equality) to 1 (complete

inequality). The larger that the coefficient is, the more unequal that

the distribution of airport seats is within the MAS.

Tables 4 and 5 present the Gini indices of the degree centrality and

traffic volume (measured by scheduled seats) for the top 10 MASs in the

world, respectively. In the case of London, where international services

control a lion’s share of the market, our analysis primarily reflect the

dynamics of its international market. The Gini indices of both degree

centrality and traffic remained relatively stable before (Q3 2019) and

during the pandemic (Q3 2022), mainly due to the lifting of travel bans

across European countries (and North America) during 2022, which led to

a recovery in the intra-European and cross-Atlantic markets. The Gini

indices of the degree of centrality and traffic in major US MASs,

including New York, Los Angeles, and Chicago, as of Q3 2022, did not

change significantly compared with those in Q3 2019. This finding

demonstrates that the network and traffic distributions of US MASs were

relatively stable once the pandemic was contained and travel

restrictions were lifted. This pattern also applies to MASs in Paris.

However, for Istanbul, we observe a more unevenly distributed degree of

centrality in the domestic market during the pandemic. Istanbul Ataturk

Airport is the primary airport in this MAS, focusing on both

international and domestic markets, while Sabiha Gokcen Airport mainly

serves the domestic market through LCC services. Prior to the pandemic,

55% of domestic traffic was served by Sabiha Airport. However, with the

pandemics impact, Sabiha Gokcen Airport withdrew some domestic routes,

resulting in a decrease in domestic traffic to a level close to that of

Ataturk Airport.

Table 4: Gini index of the degree centrality before (Q3 2019) and during late stage of pandemic (Q3 2022) for top 10 MASs

Notes:

l. The “before" represents the Q3 of 2019, and "late stage" represents

Q3 of 2022. For Hong Kong

MAS, it only constitutes Hong Kong and Shenzhen airports.

2.The rank of the airports are defined by the total scheduled seats of

the MAS at Q3, 2019.

Conversely, the MASs in Asia have experienced significant changes in

the Gini indices of degree centrality and traffic before and during the

late stage of the pandemic. In the case of the Tokyo MAS, Tokyo Narita

Airport primarily serves the international market, accounting for 67% of

international traffic as of Q3 2019. Haneda Airport, in contrast,

focuses mainly on the domestic market, serving 90% of domestic traffic

in the same period. Japan adopted stricter travel bans than European and

North American countries, with Narita Airport being affected

particularly strongly, resulting in a significant decrease in its

international degree centrality, from 120 in 2019 to 71 in 2022.

Consequently, the difference in international degree centrality between

Narita and Haneda decreased during the pandemic, leading to a 25%

decrease in the Gini index of degree centrality in the international

market. Although the number of international routes from Narita

decreased significantly, the airport’s dominance in the international

market led to an increase in the proportion of international traffic

served, resulting in a 10% increase in the Gini index of traffic. Such

findings are consistent with the empirical evidence of Ng et al. (2022),

who indicated that the Japanese airline market was heavily affected by

the pandemic, with the two dominant airlines (All Nippon Airways and

Japanese Airlines) strengthening their competition in the major domestic

routes linking to Haneda and Narita airports.

In the case of Shanghai, both Pudong and Hongqiao airports serve a

considerable number of domestic destinations. However, Hongqiao Airport

serves only a small number of international destinations, mainly

short-haul flights to Japan and Southeast Asia, while almost all

international flights are served by Pudong Airport. During the pandemic,

Pudong Airport had more under-utilized slots due to Chinas

implementation of strict bans on international airline services. As a

result, Pudong added flights to more domestic destinations, further

exceeding Hongqiao in degree centrality in the domestic market. Since

Hongqiao previously dominated the domestic traffic volume, the rise of

Pudong Airport in domestic services narrowed the domestic traffic

imbalance during the pandemic, leading to a 58% reduction in the Gini

index of domestic traffic. For Hong Kong, the Chinese government banned

flights between Hong Kong and mainland China, resulting in a significant

drop in the number of domestic routes and traffic at Hong Kong Airport,

increasing the Gini indices of domestic degree centrality and traffic of

the MAS by 63% and 75%, respectively. Shenzhen cut almost all

international flights during the pandemic, while Hong Kong maintained

more international flight services, further exacerbating the uneven

distribution of international air services in this MAS.

The Gini indices of degree centrality and traffic for the other

sampled MASs are compiled in Appendix Tables 8 and 9, respectively.

Overall, the observations indicate that, for European and US airports,

the overall inequality of traffic and degree centrality did not change

significantly by the end of 2022 compared to pre-pandemic conditions,

because domestic traffic and international traffic volumes recovered in

a similar pattern. In contrast, for the Asian Pacific MASs, the stricter

international air travel bans adopted by these countries were more

strict and lasted for much longer periods, which led to a significant

redistribution of traffic and networks in the international markets. As

airports with more idle slots from international operations switched to

domestic flight services, the intra-MAS distribution of domestic

operations also underwent significant changes.

Table 4: Gini index of the traffic (scheduled seats) before (Q3 2019) and during late stage of the pandemic (Q3 2022) for

top 10 MASs

Notes:

l. The “before" represents the Q3 of 2019, and "late stage" represents

Q3 of 2022. For Hong Kong

MAS, it only constitutes Hong Kong and Shenzhen airports.

2.The rank of the airports are defined by the total scheduled seats of

the MAS at Q3, 2019.

3.*The Hong Kong MAS includes the airports in the two nearby cities of

Hong Kong and Shenzhen.

4.2 Intra-MAS airport competition

and market overlap

In this subsection, we focus on the origin-destination (OD) level

competition among different airports within one MAS. That is, the

different airports in one MAS might offer direct flights to the same

destination. The intra-MAS airport competition is fiercer when airports

serve more overlapping destination markets. To more accurately capture

such intra-MAS competition (degree of market overlap), we devise with

the following Herfindahl-Hirschman (HHI) index on each route originating

from one MAS: OD\_HHI_Mj = ålimits_i=1m

((q_ij Q_Mj )2 where QMj is

the total scheduled seats from MASM to destination airport j; qij is

the scheduled seats from airport i in the MAS to destination airport

j; and m is the number of airports in MAS

M. Then, for each sample MAS,

we are able to calculate this HHI index for each OD market. A larger

value of HHI suggests higher market concentration, or more dominance of

the leading airport(s) within the MAS serving this OD market.

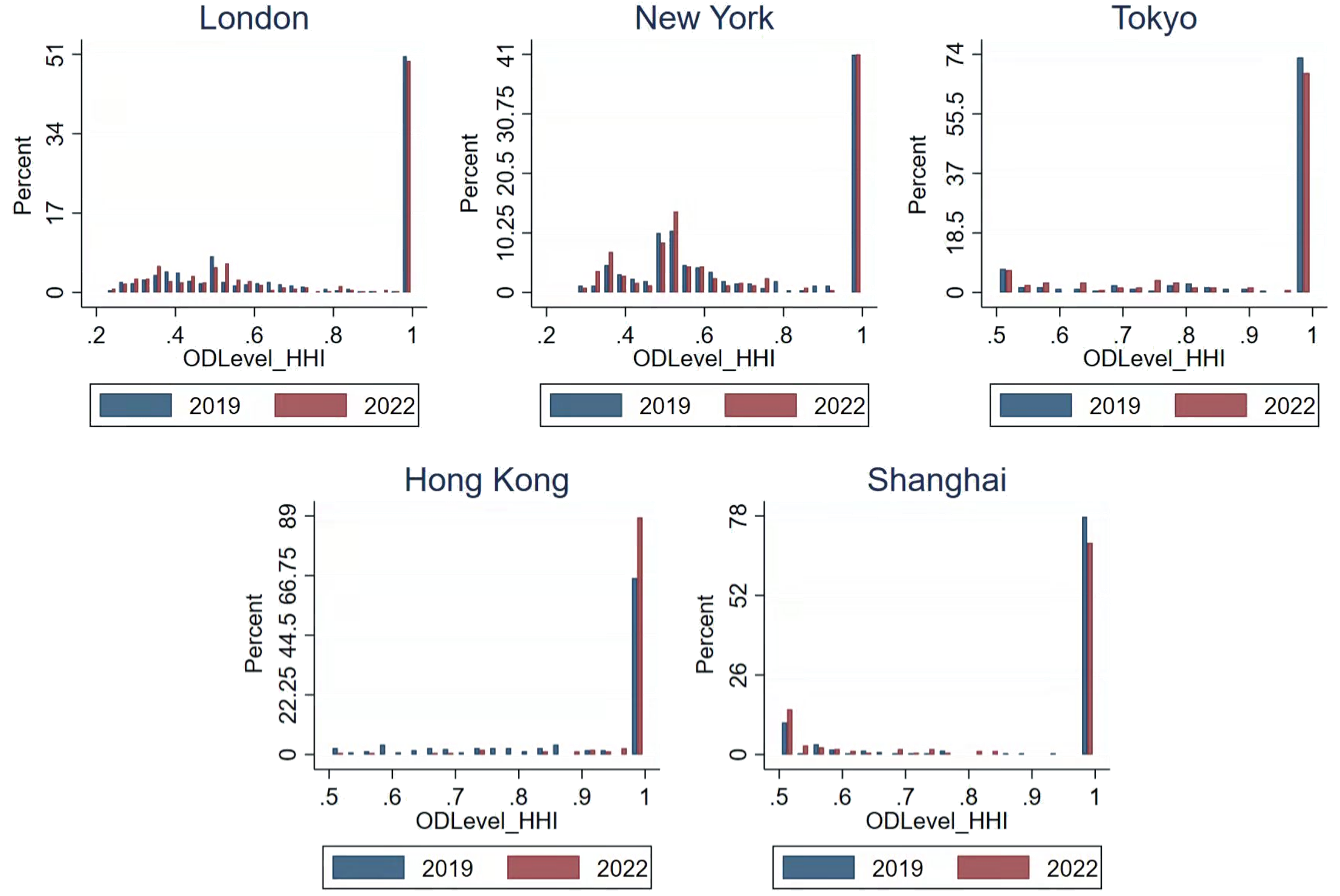

For our empirical investigation, we focus on the top 5 MASs

worldwide, namely London, New York, Tokyo, Hong Kong, and Shanghai.

These MASs are distributed in major regions around the world. In

Figure 1 and Figure 2, we present

the percentage distributions of the OD level HHIs, as calculated in Eq.

(2). For the London MAS, the HHI index became more concentrated towards

lower values, indicating more intense competition among different

airports in the London MAS. As we discuss in more detail in the next

subsection, British Airways dominated at London Heathrow Airport, while

LCC Easyjet operated its base airport at London Gatwick Airport. During

the pandemic, British Airways relocated its capacity from

intercontinental routes to more intra-European routes at its Heathrow

hub, leading to more head-to-head competition with Easyjet at London

Gatwick. For the New York MAS, there was no significant change in the OD

level HHI during the pandemic. This outcome can be attributed to the

almost full recovery of the US aviation market in Q3 2022 compared with

Q3 2019, with airlines returning service levels and network

configurations to pre-pandemic levels. In other words, we did not

observe any clear or long-term changes in the MAS structure caused by

the pandemic in the US.

In the case of the Tokyo MAS, the intra-MAS competition between

Narita and Haneda airports appeared to intensify, with an overall

decrease in the OD level HHI. This result occurred primarily because,

during the pandemic, both airports cut services in thin markets and

focused on denser and more lucrative routes, enhancing their market

overlap and head-to-head competition. For the Hong Kong MAS, both the

Hong Kong and Shenzhen airports were heavily impacted during the

pandemic. Before the pandemic, they served many common destinations in

mainland China, as well as short- to medium-haul international routes.

However, most of the flights from Hong Kong to mainland Chinese cities

were suspended during the pandemic, and international flights from

Shenzhen were also dramatically reduced. Consequently, the two airports

networks became very distinct during the pandemic. Last, in the case of

the Shanghai MAS, the competition between the Hongqiao and Pudong

airports became much more intense. As discussed in the previous

subsection (4.1), to alleviate the adverse impact of the pandemic,

Pudong Airport expanded its domestic market services, resulting in

increased head-to-head competition with Hongqiao Airport in many

domestic OD markets.

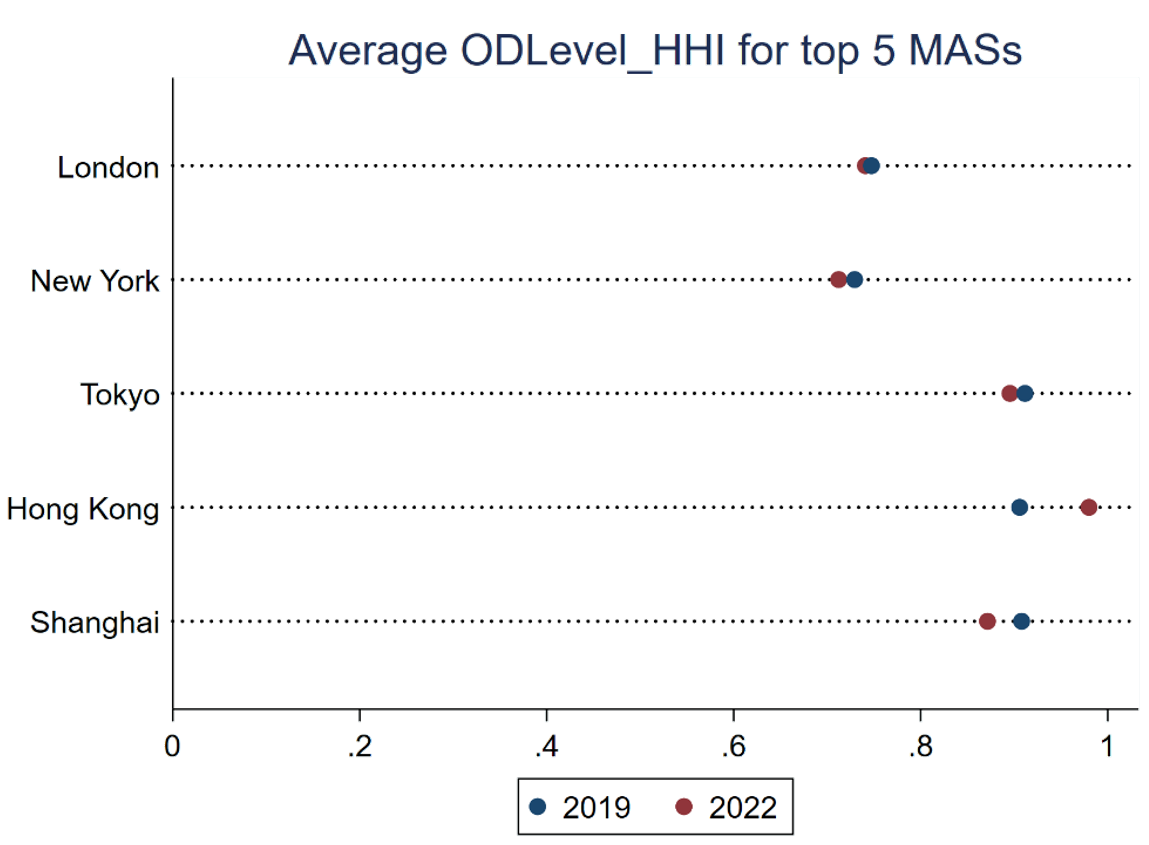

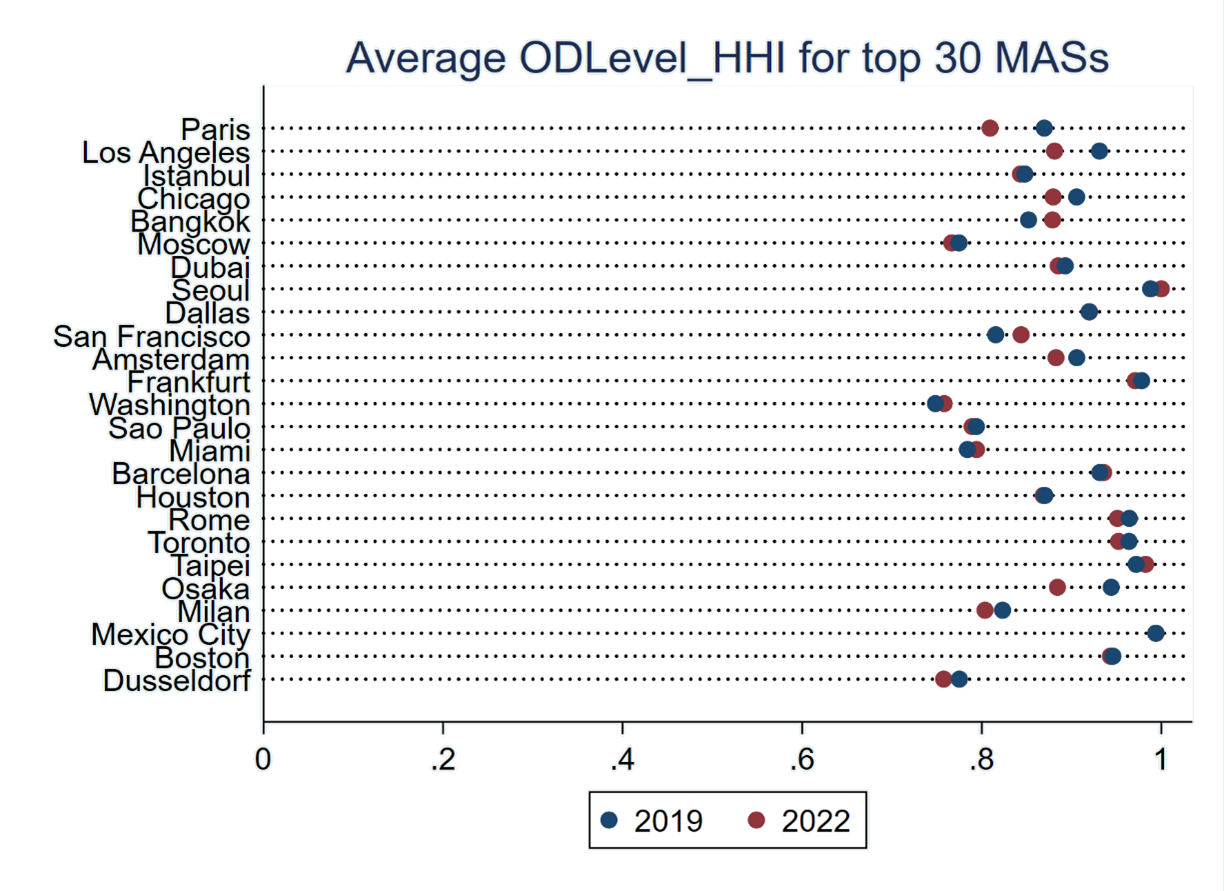

We also calculated the average OD level HHI for each MAS to provide

an overall measure of changes in airport competition within the MAS (as

illustrated in Figure 2). Except for the Hong Kong MAS, all four of the

other systems experienced increased intra-MAS airport competition during

the later stage of the pandemic, consistent with our earlier

analysis.

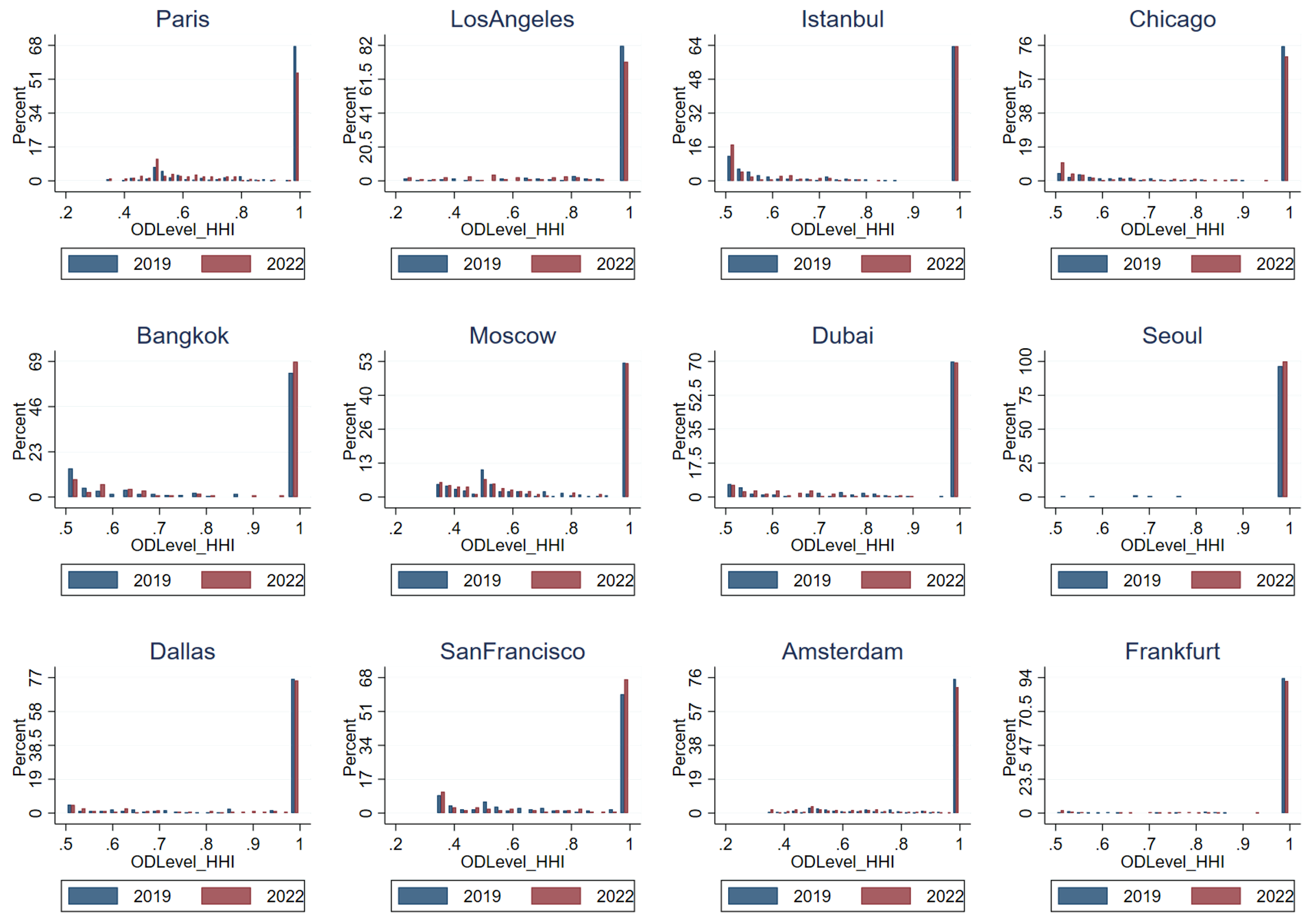

Furthermore, we compiled the distribution of the OD level HHI and

average OD level HHI before and during the late stage of the pandemic

for other sampled MASs and we present the results for the top 30 MASs in

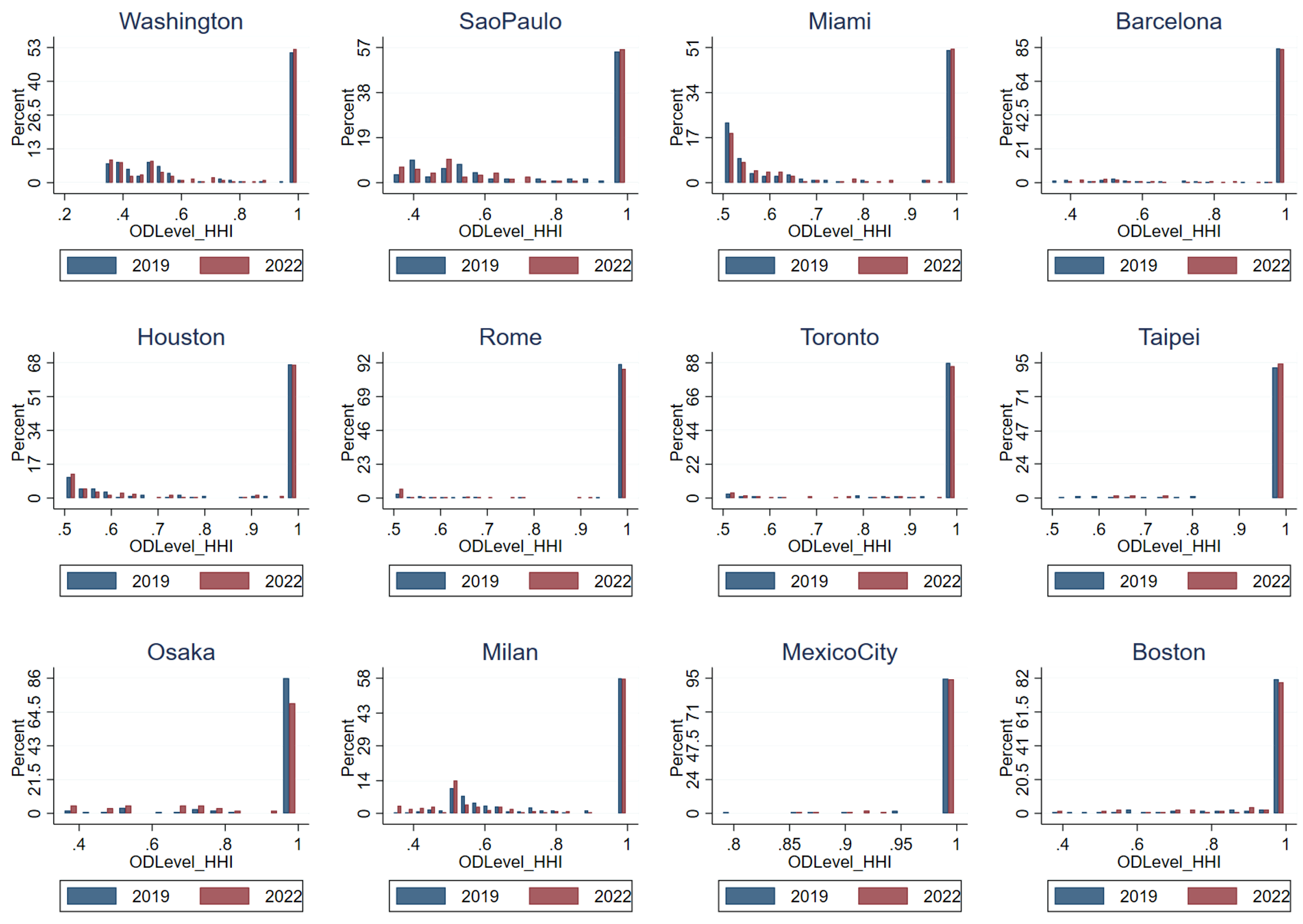

Figures 3 and 4. Overall, the observations indicate that for US and

European MASs, once travel bans were lifted, the intra-MAS airport

competition structure returned to pre-pandemic levels. In contrast, for

Asian Pacific MASs, intra-MAS airport competition could be significantly

reshaped because relevant airports operations had been significantly

constrained by strict international air travel bans.

Figure 1: The distribution of OD HHI for top 5 MAS before

(Q3 2019) and during late stage of pandemic (Q3 2022). Figure 2: The Average OD HHI for top 5 MASs before (Q3 2019)

and during late stage of pandemic (Q3 2022).

4.3 Airline competition within the

MAS

In this subsection, we examine the impact of the pandemic on

airline-level competition within MASs. First, to measure the overall

airline competition intensity, we calculate the airline HHI in each MAS

using the following equation. Airline\_HHI_M = ålimits_i=1N

((q_iM Q_M )2 where qiM is

the scheduled seats of airline i in MAS M, regardless of airport; QM is the total

scheduled seats in MAS M; and

N is the number of airlines in

MAS M. A larger value of

airline HHI suggests more dominance of particular airlines within one

MAS. Table 6 summarizes the airline HHIs for the top 10 MASs before and

during the late stage of the pandemic. For US and European MASs, the

airline HHI did not change significantly. This outcome suggests that

there were no significant airline exits in these MASs during the

pandemic. While some airlines might have exited the market in the early

stages of the pandemic, once it was under control and most travel bans

were lifted, airline services resumed quickly, leading to similar

airline concentration levels. In contrast, for Asia-Pacific MASs, the

concentration level of airlines increased significantly, with some

airlines becoming much more dominant during the pandemic. One possible

explanation is the crowding effect imposed by large-sized dominant

airlines. Since international flight services were largely suspended,

airlines that previously served international markets redeployed their

capacity in domestic markets, intensifying competition and leading to

exits by small airlines and LCCs. The MASs thus became more

concentrated. We also compiled the airline HHI results for other MASs in

Appendix Table 10. Notably, for small-scale MASs, such as Milan, Venice,

and Bologna, their airline HHIs also increased significantly due to

economies of scale. With air traffic dropping during the pandemic, it

was difficult for all airlines to achieve efficient operations, and some

inefficient airlines exited the market, leading to a higher airline

HHI.

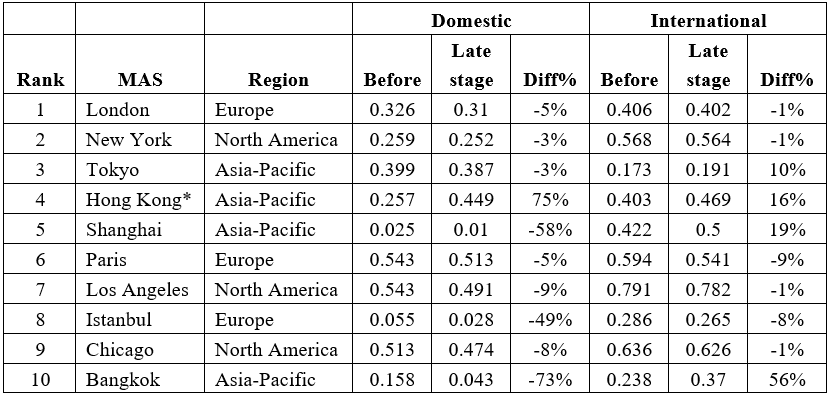

Table 6: Airline HHI of top 10 MASs before (Q3 2019) and during late

stage of pandemic (Q3 2022)

Rank

MAS

Before

Late stage

Diff%

1

London

0.118

0.115

-3%

2

New York

0.139

0.151

9%

3

Tokyo

0.183

0.235

28%

4

Hong Kong

0.079

0.123

55%

5

Shanghai

0.125

0.155

24%

6

Paris

0.176

0.177

0%

7

Los Angeles

0.118

0.124

5%

8

Istanbul

0.456

0.486

6%

9

Chicago

0.238

0.234

2%

10

Bangkok

0.080

0.080

0%

Notes:

l. The “before" represents the Q3 of 2019, and "late stage" represents

Q3 of 2022. For Hong Kong

MAS, it only constitutes Hong Kong and Shenzhen airports.

2.The rank of the airports are defined by the total scheduled seats of

the MAS at Q3, 2019.

In addition to overall airline concentration, we also investigated

competition between FSCs and LCCs in MASs. In some MASs, FSCs and LCCs

prefer to have hubs at different airports. For example, in the London

MAS, British Airways (FSC) has its hub at Heathrow Airport, while

Easyjet has its main base at Gatwick Airport. In other MASs, FSCs and

LCCs are not clearly distinguished in hub airports. For instance, in the

Shanghai MAS, Spring Airlines (a LCC) and China Eastern Airlines (a FSC)

claim hubs at both Hongqiao and Pudong airports. Spring Airlines aims to

enter both airports to attract passengers with different airport

preferences in the MAS, but doing so could hinder their achievement of

economies of scale. The pandemic might have affected the incentives of

FSCs and LCCs to choose airport entry and capacity distribution in the

MAS. Thus, we calculated the Gini index of LCC capacity share, and the

results for the top 10 MASs are shown in Table 7. First, for European

and US MASs, the LCC capacity share became slightly more balanced during

the pandemic, as indicated by an overall decrease in the Gini index.

This outcome suggests that LCCs preferred to maintain the presence at

multiple airports in MASs to serve passengers that have different

airport preferences. This is probably due to LCCs’ significant market

shares and traffic volumes, which enable them to maintain sizeable

operations at multiple airports. This is helped by the fact that LCCs

offer simplified services (e.g. no connection nor complicated baggage

handling, simple catering services), thus not too costly to maintain

operations at multiple airports.

However, for Asia-Pacific MASs, particularly the Shanghai MAS, LCCs

preferred to concentrate operations in a single airport, Pudong Airport,

during the pandemic. There are two possible rationales for this choice.

First, LCCs have a much smaller presence and market occupation in China

and Japan, especially in China (no more than 15%). Therefore, it is

crucial for them to have sufficient traffic to achieve economies of

scale, especially when many input prices are beyond the control of LCCs

(Fu et al. 2015b; Su et al. 2020). When the market is in a downturn and

the traffic volume is low, LCCs must consolidate traffic into one

airport in the MAS to maintain a certain level of operational scale. Our

data show that Chinas largest LCC, Spring Airlines, increased its market

share at Pudong Airport more than at Hongqiao Airport during the

pandemic. When more idle slots are available for redistribution, LCCs

can acquire them and expand services, in line with Chinas policy

allowing LCCs to obtain new slots and open new routes from major hub

airports (Shanghai and Beijing) during the pandemic as an indirect

measure to support private LCCs in surviving the market downturn (e.g.,

Hou et al., 2021). Second, FSCs in the Asia-Pacific region faced more

restrictive bans on operating international markets, forcing them to

compete more aggressively in the domestic market to survive. They

attempted to prevent LCC expansion in their hub airports by adopting

more aggressive competition strategies, such as deep price discounts.

The Gini index of LCC capacity share for other MASs is available in

Appendix Table 11.

Table 7: Gini index of LCC capacity share in top 10 MASs before (Q3

2019) and during late stage of pandemic (Q3 2022)

Rank

MAS

Before

Late stage

Diff%

1

London

0.461

0.437

-5%

2

New York

0.428

0.379

-11%

3

Tokyo

0.269

0.332

23%

4

Hong Kong

0.148

0.190

28%

5

Shanghai

0.026

0.069

169%

6

Paris

0.321

0.290

-10%

7

Los Angeles

0.247

0.209

-15%

8

Istanbul

0.467

0.489

5%

9

Chicago

0.309

0.296

-4%

10

Bangkok

0.385

0.282

-27%

Notes:

l. The “before" represents the Q3 of 2019, and "late stage" represents

Q3 of 2022. For Hong Kong

MAS, it only constitutes Hong Kong and Shenzhen airports.

2.The rank of the airports are defined by the total scheduled seats of

the MAS at Q3, 2019.

5 Conclusions

This study first reviewed and summarized the recent literature on

MASs, discussing the main research topics and development patterns. It

is noted that the impacts of the pandemic on MASs have not been well

explored in the literature. Therefore, we collected

airport-airline-specific capacity data from OAG (before and during the

late stage of the pandemic) to examine the pandemics impact on different

dimensions of MAS operations worldwide following the definitions used in

previous studies for consistency. A total of 53 MASs are included in our

sample, with a focus on the top MASs around the world. By calculating

descriptive statistics and indices, we studied three dimensions of MAS

structures before and during the late stage of the pandemic: i) traffic

and degree centrality distributions within MASs; ii) intra-MAS airport

competition (the degree of OD market overlap); and iii) airline

competition intensity within MASs.

Our statistics suggest heterogeneous impacts of the pandemic on MASs

in different regions when comparing market outcomes between Q3 2019

(before the pandemic) and Q3 2022 (during the pandemic). For MASs in the

US and Europe, the distribution of traffic and degree centrality among

airports remained largely unchanged. Both the domestic and international

airline markets in these MASs have returned to pre-pandemic levels at

similar paces. Until the end of 2022, intra-MAS airport competition and

airline airport dominance and concentration (including between FSCs and

LCCs) have also been similar to pre-pandemic levels at major European

and US MASs. These results suggest the stability of MAS structures in

the US and Europe after their airline markets recovered from the

unprecedented shock of the pandemic.

In contrast, Asia-Pacific MASs experienced significant changes during

the pandemic, mainly due to very restrictive bans on international

travel. Since large-sized airlines could not serve international

markets, they had to redeploy their capacity into domestic markets,

leading to significant changes in the MAS structure. First, airport

traffic could be more balanced within the MAS, and intra-MAS airport

competition became much fiercer as airports focused on operations in

similar domestic destinations. On the other hand, smaller airlines

dropped quite a few markets, leading to higher airline concentration

levels. The net effect (i.e. whether competition in an MAS increased and

decreased) remains unclear. It is also noted that LCCs in Asia-Pacific

seemed more likely to have a main base in a single airport in one MAS,

either due to the incentive of achieving economies of scale or they were

pushed out from other airports due to stronger competitive responses

from FSCs who were forced to allocate more capacity to domestic

markets.

In general, our study identified heterogeneous development and

recovery patterns among MASs in different regions. Although some

possible explanations are proposed, more in-depth analysis is required

to go beyond simple statistics. Our study also raised some questions

unanswered. For example, government interventions in the European and

North American markets, where market largely returned to pre-pandemic

conditions, are probably not necessary. Yet it is not clear whether the

any government intervention should be considered to address the

heterogeneous impacts caused by the pandemic, especially for

“distortions” caused by previous regulations (e.g. ban on international

services). Extension studies based on updated data can be helpful in

addressing those important questions.

References

Babić, D., Kalić, M., Janić, M., Dožić, S., & Kukić, K. (2022).

Integrated Door-to-Door Transport Services for Air Passengers: From

Intermodality to Multimodality. Sustainability, 14(11), 6503.

Bezerra, G. C., & Gomes, C. F. (2019). Determinants of passenger

loyalty in multi-airport regions: Implications for tourism

destination. Tourism Management Perspectives, 31, 145-158.

Bonnefoy, P. A., de Neufville, R., & Hansman, R. J. (2010).

Evolution and development of multiairport systems: Worldwide

perspective. Journal of Transportation Engineering, 136(11),

1021-1029.

Brueckner, J. K. (2003). Airline traffic and urban economic

development. Urban Studies, 40(8), 1455-1469.

Chen, T., Fu, X., Hensher, D. A., Li, Z. C., & Sze, N. N.

(2022a). Air travel choice, online meeting and passenger

heterogeneity–An international study on travellers’ preference during a

pandemic. Transportation Research Part A: Policy and Practice, 165,

439-453.

Chen, T., Fu, X., Hensher, D., Li, Z.C., Sze, N.N., (2022b), The

effect of online meeting and health screening on business travel: a

stated preference case study in Hong Kong, Transportation Research -

Part E , 164, 102823.

Cheung, T. K.-Y., Wong, W.-h., Zhang, A., & Wu, Y. (2020).

Spatial panel model for examining airport relationships within

multi-airport regions. Transportation Research Part A: Policy and

Practice, 133, 148-163.

Chiambaretto, P., Baudelaire, C., & Lavril, T. (2013). Measuring

the willingness-to-pay of air-rail intermodal passengers. Journal of Air

Transport Management, 26, 50-54.

Czerny, A. I., Fu, X., Lei, Z., & Oum, T. H. (2021). Post

pandemic aviation market recovery: Experience and lessons from

China. Journal of Air Transport Management, 90, 101971.

de Neufville, R. (2004). The Future of Secondary Airports: Nodes of a

parallel air transport network?

de Neufville, R. (2016). Multi-Airport Systems. Istanbul Technical

University. Air Transportation Management. Airport Planning and

Management. Module 24.

de Paula Balan, B., da Cunha, M. C. F., da Cunha, R. C., &

Halawi, L. (2022) Aviation supply and demand in the São Paulo and Rio de

Janeiro systems evolution: An exploratory study. Journal of Economics

and Management, 44(1), 393-419.

Fu, X., Dresner, M. & Oum, T.H. (2011), Effects of transport

service differentiation in the U.S. domestic airline market,

Transportation Research – Part E 47(3), 297-305.

Fu X., Lei Z., Wang K. and Yan J. (2015b), Low cost carrier

competition and route entry in an emerging but regulated aviation market

- the Case of China, Transportation Research - Part A, 79, 3-16.

Fu, X., Jin, H., Liu, S., Oum, T.H., & Yan, J. (2019) Exploring

network effects of Point-to-Point networks: An investigation of the

spatial patterns of Southwest airlines’ network, Transport Policy, 76,

36-45.

Fu X., Oum T.H., Chen R. & Lei Z. (2015a), Dominant carrier

performance and international liberalization – the case of North East

Asia, Transport Policy, 43, 61–75.

Fuellhart, K., O’Connor, K., & Woltemade, C. (2013). Route-level

passenger variation within three multi-airport regions in the

USA. Journal of Transport Geography, 31, 171-180.

Harvey, G. (1987). Airport choice in a multiple airport

region. Transportation Research Part A: General, 21(6), 439-449.

Hess, S., & Polak, J. W. (2006). Exploring the potential for

cross-nesting structures in airport-choice analysis: a case-study of the

Greater London area. Transportation Research Part E: Logistics and

Transportation Review, 42(2), 63-81.

Hou, M., Wang, K., & Yang, H. (2021). Hub airport slot

Re-allocation and subsidy policy to speed up air traffic recovery amid

COVID-19 pandemic---case on the Chinese airline market. Journal of Air

Transport Management, 93, 102047.

Hou, M., Wang, K., Yang, H., & Zhang, A. (2022). Airport-airline

Relationship, Competition and Welfare in a Multi-airport System: The

Case of New Beijing Daxing Airport. Journal of Transport Economics and

Policy (JTEP), 56(2), 156-189.

Jung, S.-Y., & Yoo, K.-E. (2016). A study on passengers airport

choice behavior using hybrid choice model: A case study of Seoul

metropolitan area, South Korea. Journal of Air Transport Management, 57,

70-79.

Kuo, P.-F., Putra, I. G. B., Setiawan, F. A., Wen, T.-H., Chiu,

C.-S., & Sulistyah, U. D. (2022). The impact of the COVID-19

pandemic on OD flow and airport networks in the origin country and in

Northeast Asia. Journal of Air Transport Management, 100, 102192.

Li, L. Y., Mao, Y. J., Wang, Y., & Ma, Z. H. (2022). How has

airport service quality changed in the context of COVID-19: A

data-driven crowdsourcing approach based on sentiment analysis. Journal

of Air Transport Management, 105.

Li, S. P., Zhou, Y. M., Kundu, T., & Sheu, J. B. (2021).

Spatiotemporal variation of the worldwide air transportation network

induced by COVID-19 pandemic in 2020. Transport Policy, 111,

168-184.

Li, X., Tang, J., Hu, X., & Wang, W. (2020). Assessing intercity

multimodal choice behavior in a Touristy City: A factor analysis.

Journal of Transport Geography, 86, 102776.

Li, Z.-C., Tu, N., Fu, X., & Sheng, D. (2022). Modeling the

effects of airline and high-speed rail cooperation on multi-airport

systems: The implications on congestion, competition and social welfare.

Transportation Research Part B-Methodological, 155, 448-478.

Liao, W., Cao, X., & Li, S. (2019). Competition and

Sustainability Development of a Multi-Airport Region: A Case Study of

the Guangdong-Hong Kong-Macao Greater Bay Area. Sustainability,

11(10).

Liao, W., Cao, X., Liu, Y., & Huang, Y. (2022). Investigating

differential effects of airport service quality on behavioral intention

in the multi-airport regions. Research in Transportation Business &

Management, 45, 100877.

Ma, G. F., Ding, Y., & Ma, J. Y. (2022). The Impact of Airport

Physical Environment on Perceived Safety and Domestic Travel Intention

of Chinese Passengers during the COVID-19 Pandemic: The Mediating Role

of Passenger Satisfaction. Sustainability, 14(9).

Mamdoohi, A. R., Yazdanpanah, M., Taherpour, A., & Saffarzadeh,

M. (2014). An analysis of resident and Non-resident air passenger

behaviour of origin airport choice. International Journal of

Transportation Engineering, 2(1), 13-30.

Marcucci, E., & Gatta, V. (2011). Regional airport choice:

Consumer behaviour and policy implications. Journal of Transport

Geography, 19(1), 70-84.

Marcucci, E., & Gatta, V. (2012). Dissecting preference

heterogeneity in consumer stated choices. Transportation Research Part

E: Logistics and Transportation Review, 48(1), 331-339.

Monmousseau, P., Marzuoli, A., Feron, E., & Delahaye, D. (2020).

Impact of Covid-19 on passengers and airlines from passenger

measurements: Managing customer satisfaction while putting the US Air

Transportation System to sleep. Transportation Research

Interdisciplinary Perspectives, 7, 100179.

Mueller, F. (2022). Examining COVID-19-triggered changes in spatial

connectivity patterns in the European air transport network up to June

2021. Research in Transportation Economics, 94, 101127.

Murça, M. C. R., & Correia, A. R. (2013). Análise da modelagem da

escolha aeroportuária em regiões de múltiplos aeroportos.

[Analysis of airport choice modeling in multi-airport

regions]. Journal of Transport Literature, 7(4),

130-146.

Nižetić, S. (2020). Impact of coronavirus (COVID‐19) pandemic on air

transport mobility, energy, and environment: A case study. International

Journal of Energy Research, 44(13), 10953-10961.

Noruzoliaee, M., Zou, B., & Zhang, A. (2015). Airport partial and

full privatization in a multi-airport region: Focus on pricing and

capacity. Transportation Research Part E: Logistics and Transportation

Review, 77, 45-60.

Ng, K. T., Fu, X., Hanaoka, S., & Oum, T. H. (2022). Japanese

aviation market performance during the COVID-19 pandemic-Analyzing

airline yield and competition in the domestic market. Transport

Policy, 116, 237-247.

Paliska, D., Drobne, S., Borruso, G., Gardina, M., & Fabjan, D.

(2016). Passengers airport choice and airports catchment area analysis

in cross-border Upper Adriatic multi-airport region. Journal of Air

Transport Management, 57, 143-154.

Pels, E., Nijkamp, P., & Rietveld, P. (2000). Airport and airline

competition for passengers departing from a large metropolitan area.

Journal of Urban Economics, 48(1), 29-45.

Pels, E., Nijkamp, P., & Rietveld, P. (2001). Airport and airline

choice in a multiple airport region: an empirical analysis for the San

Francisco Bay Area. Regional Studies, 35(1), 1-9.

Pels, E., Nijkamp, P., & Rietveld, P. (2003). Access to and

competition between airports: a case study for the San Francisco Bay

area. Transportation Research Part A: Policy and Practice, 37(1),

71-83.

Salesi, V. K., Tsui, W. H. K., Fu, X., & Gilbey, A. (2022).

Strategies for South Pacific Region to address future pandemics:

Implications for the aviation and tourism sectors based on a systematic

literature review (2010–2021). Transport Policy.

Shamohammadi, M., Park, Y., Choi, J. H., & Kwon, O. K. (2022).

Exploring the Performance of International Airports in the Pre- and

Post-COVID-19 Era: Evidence from Incheon International Airport.

Sustainability, 14(7).

Sheard, N. (2014). Airports and urban sectoral employment. Journal of

Urban Economics, 80, 133-152.

Su, M., Luan, W., Fu, X., Yang, Z., Zhang, R. (2020) The competition

effects of low-cost carriers and high-speed rail on the Chinese aviation

market, Transport Policy, 95, 37-46.

Sun, X., Wandelt, S., Hansen, M., & Li, A. (2017). Multiple

airport regions based on inter-airport temporal distances.

Transportation Research Part E: Logistics and Transportation Review,

101, 84-98.

Sun, X., Wandelt, S., & Zhang, A. (2020). How did COVID-19 impact

air transportation? A first peek through the lens of complex networks.

Journal of Air Transport Management, 89, 101928.

Sun, X., Wandelt, S., & Zhang, A. (2021b). On the degree of

synchronization between air transport connectivity and COVID-19 cases at

worldwide level. Transport Policy, 105, 115-123.

Sun, X., Wandelt, S., Zheng, C., & Zhang, A. (2021a). COVID-19

pandemic and air transportation: Successfully navigating the paper

hurricane. Journal of Air Transport Management, 94, 102062.

Sun, X., Wandelt, S., & Zhang, A. (2022). COVID-19 pandemic and

air transportation: Summary of Recent Research, Policy Consideration and

Future Research Directions. Transportation Research Interdisciplinary

Perspectives, 16, 100718.

Suzumura, T., Kanezashi, H., Dholakia, M., Ishii, E., Napagao, S. A.,

Pérez-Arnal, R., & Garcia-Gasulla, D. (2020). The impact of COVID-19

on flight networks. In 2020 IEEE International Conference on Big Data

(Big Data) (pp. 2443-2452). IEEE.

Teixeira, F. M., & Derudder, B. (2021). Spatio-temporal dynamics

in airport catchment areas: The case of the New York Multi Airport

Region. Journal of Transport Geography, 90, 102916.

Tiglao, N. C. Investigating Tourists’ Airport Choice in the

Multi-Airport Region of Aklan, Philippines and Its Implications on

Airport Capacity Expansion Decisions. Transport, 3(1).

Tu, N., Li, Z.C., Fu, X., Lei, Z. (2020). Airline network competition

in inter-continental market. Transportation Research - Part E, 143,

102117.

Wang K., Gong Q., Fu X. and Fan X. (2014), Frequency and aircraft

size dynamics in a concentrated growth market: The case of the Chinese

domestic market, Journal of Air Transport Management, 36, 50–58.

Wang, K., Tsui, K., Li, L.B., Lei, Z., Fu, X. (2020b) Entry pattern of

low-cost carriers in New Zealand - The impact of domestic and

trans-Tasman market factors, Transport Policy, 93, 36-45.

Wang, K., Jiang, C., Ng, A. K., & Zhu, Z. (2020a). Air and rail

connectivity patterns of major city clusters in China. Transportation

Research Part A: Policy and Practice, 139, 35-53.

Wong, W. H., Cheung, T., Zhang, A., & Wang, Y. (2019a). Is

spatial dispersal the dominant trend in air transport development? A

global analysis for 2006-2015. Journal of Air Transport Management, 74,

1-12.

Wong, W.-H., Zhang, A., Cheung, T. K.-Y., & Chu, J. (2019b).

Examination of low-cost carriers development at secondary airports using

a comprehensive world airport classification. Journal of Air Transport

Management, 78, 96-105.

Winston, C., & Yan, J. (2011). Can privatization of US highways

improve motorists welfare?. Journal of Public Economics, 95(7-8),

993-1005.

Yan, J., & Winston, C. (2014). Can private airport competition

improve runway pricing? The case of San Francisco Bay area airports.

Journal of Public Economics, 115, 146-157.

Zhang, A. (1996) An analysis of fortress hubs in airline networks,

Journal of Transport Economics and Policy, 30(3), 293-307.

Zhang, L., Hou, M., Liu, Y., Wang, K., & Yang, H. (2022). Measuring Beijing's international air connectivity and suggestions for improvement post COVID-19. Transport Policy, 116, 132-143.

Zhang, L., Yang, H., Wang, K., Bian, L., & Zhang, X. (2021). The

impact of COVID-19 on airline passenger travel behavior: An exploratory

analysis on the Chinese aviation market. Journal of Air Transport

Management, 95, 102084.

Zhang, Y., Zhang, A., & Wang, J. (2020). Exploring the roles of

high-speed train, air and coach services in the spread of COVID-19 in

China. Transport Policy, 94, 34-42.

Appendix

Table 8: Gini index of the degree centrality before (Q3 2019) and during

late stage of pandemic (Q3 2022) for MASs (other than top 10

MASs)

Domestic

International

Rank

MAS

Region

Before

Late stage

Diff%

Before

Late stage

Diff%

11

Moscow

Europe

0.017

0.038

118%

0.116

0.08

-31%

12

Dubai

Latin America & Middle East

0

0

NA

0.223

0.224

0%

13

Seoul

Asia-Pacific

0.25

0.389

56%

0.464

0.48

3%

14

Dallas

North America

0.256

0.226

-12%

0.5

0.5

0%

15

San Francisco

North America

0.138

0.214

55%

0.387

0.437

13%

16

Amsterdam

Europe

0.133

0

-100%

0.389

0.345

-11%

17

Frankfurt

Europe

0.5

0.5

0%

0.395

0.38

-4%

18

Washington

North America

0.04

0.053

34%

0.438

0.433

-1%

19

Sao Paulo

Latin America & Middle East

0.106

0.164

55%

0.583

0.623

7%

20

Miami

North America

0.087

0.007

-92%

0.145

0.147

2%

21

Barcelona

Europe

0.667

0.586

-12%

0.403

0.426

6%

22

Houston

North America

0.18

0.15

-17%

0.359

0.361

1%

23

Rome

Europe

0.462

0.423

-8%

0.281

0.33

17%

24

Toronto

North America

0.381

0.292

-23%

0.603

0.604

0%

25

Taipei

Asia-Pacific

0.5

0.5

0%

0.407

0.442

9%

26

Osaka

Asia-Pacific

0.294

0.226

-23%

0.667

0.667

0%

27

Milan

Europe

0.026

0.062

137%

0.32

0.267

-17%

28

Mexico City

Latin America & Middle East

0.398

0.357

-10%

0.5

0.5

0%

29

Boston

North America

0.381

0.384

1%

0.642

0.667

4%

30

Dusseldorf

Europe

0.513

0.437

-15%

0.352

0.307

-13%

31

Orlando

North America

0.051

0.057

11%

0.312

0.438

40%

32

Manchester

Europe

0.292

0.232

-20%

0.278

0.271

-3%

33

Vienna

Europe

0.5

0.3

-40%

0.272

0.302

11%

34

Brussels

Europe

0

0

NA

0.383

0.319

-17%

35

Detroit

North America

0.451

0.394

-13%

0.5

0.433

-13%

36

Melbourne

Asia-Pacific

0.409

0.435

6%

0.477

0.5

5%

37

Copenhagen

Europe

0.167

0.125

-25%

0.405

0.377

-7%

38

San Diego

North America

0.142

0.132

-7%

0.318

0.5

57%

39

Philadelphia

North America

0.444

0.418

-6%

0.5

0.467

-7%

40

Oslo

Europe

0.372

0.353

-5%

0.309

0.284

-8%

41

Stockholm

Europe

0.419

0.396

-6%

0.484

0.59

22%

42

Vancouver

North America

0.304

0.394

29%

0.485

0.5

3%

43

Glasgow

Europe

0.346

0.349

1%

0.363

0.411

13%

44

Buenos Aires

Latin America & Middle East

0.255

0.11

-57%

0.456

0.125

-73%

45

Rio De Janeiro

Latin America & Middle East

0.095

0.056

-42%

0.5

0.5

0%

46

Tampa

North America

0.188

0.116

-38%

0.615

0.476

-23%

47

Tehran

Latin America & Middle East

0.5

0.5

0%

0.5

0.479

-4%

48

Stuttgart

Europe

0.357

0.389

9%

0.26

0.223

-14%

49

Venice

Europe

0.111

0.382

244%

0.23

0.142

-38%

50

Cleveland

North America

0.339

0.266

-21%

0.5

0.5

0%

51

Pisa

Europe

0.269

0.188

-30%

0.216

0.228

6%

52

Belfast

Europe

0.052

0.094

81%

0.438

0.469

7%

53

Norfolk

North America

0.403

0.474

18%

0

0

NA

Notes:

1.The “before” represents the Q3 of 2019, and “late stage” represents Q3

of 2022.

2.The rank of the airports are defined by the total scheduled seats of

the MAS at Q3, 2019.

Table 9: Gini index of the traffic before (Q3 2019) and during late

stage of pandemic (Q3 2022) for MASs (other than top 10 MASs)

Domestic

International

Rank

MAS

Region

Before

Late stage

Diff%

Before

Late stage

Diff%

11

Moscow

Europe

0.155

0.201

30%

0.276

0.034

-88%

12

Dubai

Latin America & Middle East

0

0

NA

0.384

0.359

-7%

13

Seoul

Asia-Pacific

0.465

0.5

8%

0.444

0.484

9%

14

Dallas

North America

0.287

0.288

0%

0.5

0.5

0%

15

San Francisco

North America

0.274

0.222

-19%

0.569

0.606

7%

16

Amsterdam

Europe

0.552

0.173

-69%

0.568

0.543

-4%

17

Frankfurt

Europe

0.5

0.5

0%

0.481

0.472

-2%

18

Washington

North America

0.108

0.128

19%

0.528

0.527

0%

19

Sao Paulo

Latin America & Middle East

0.198

0.151

-24%

0.618

0.612

-1%

20

Miami

North America

0.057

0.047

-17%

0.189

0.215

14%

21

Barcelona

Europe

0.667

0.662

-1%

0.574

0.571

-1%

22

Houston

North America

0.192

0.194

1%

0.438

0.418

-5%

23

Rome

Europe

0.486

0.473

-3%

0.382

0.4

5%

24

Toronto

North America

0.551

0.547

-1%

0.632

0.634

0%

25

Taipei

Asia-Pacific

0.5

0.5

0%

0.441

0.467

6%

26

Osaka

Asia-Pacific

0.317

0.298

-6%

0.667

0.667

0%

27

Milan

Europe

0.335

0.15

-55%

0.444

0.293

-34%

28

Mexico City

Latin America & Middle East

0.478

0.479

0%

0.5

0.5

0%

29

Boston

North America

0.542

0.543

0%

0.661

0.667

1%

30

Dusseldorf

Europe

0.524

0.567

8%

0.492

0.456

-7%

31

Orlando

North America

0.432

0.444

3%

0.467

0.494

6%

32

Manchester

Europe

0.385

0.279

-27%

0.447

0.454

2%

33

Vienna

Europe

0.5

0.497

-1%

0.428

0.431

1%

34

Brussels

Europe

0

0

NA

0.511

0.466

-9%

35

Detroit

North America

0.484

0.482

0%

0.5

0.499

0%

36

Melbourne

Asia-Pacific

0.471

0.48

2%

0.462

0.5

8%

37

Copenhagen

Europe

0.116

0.193

67%

0.47

0.468

0%

38

San Diego

North America

0.241

0.152

-37%

0.416

0.5

20%

39

Philadelphia

North America

0.472

0.459

-3%

0.5

0.494

-1%

40

Oslo

Europe

0.466

0.468

1%

0.411

0.403

-2%

41

Stockholm

Europe

0.473

0.51

8%

0.586

0.631

8%

42

Vancouver

North America

0.424

0.414

-2%

0.498

0.5

0%

43

Glasgow

Europe

0.384

0.341

-11%

0.371

0.415

12%

44

Buenos Aires

Latin America & Middle East

0.414

0.329

-21%

0.471

0.172

-63%

45

Rio De Janeiro

Latin America & Middle East

0.102

0.315

208%

0.5

0.5

0%

46

Tampa

North America

0.508

0.458

-10%

0.666

0.654

-2%

47

Tehran

Latin America & Middle East

0.5

0.5

0%

0.5

0.5

0%

48

Stuttgart

Europe

0.463

0.48

4%

0.391

0.347

-11%

49

Venice

Europe

0.172

0.426

148%

0.355

0.282

-21%

50

Cleveland

North America

0.426

0.448

5%

0.5

0.5

0%

51

Pisa

Europe

0.265

0.32

21%

0.128

0.102

-21%

52

Belfast

Europe

0.09

0.091

1%

0.437

0.457

5%

53

Norfolk

North America

0.405

0.467

15%

0

0

NA

Notes:

1.The “before” represents the Q3 of 2019, and “late stage” represents Q3

of 2022.

2.The rank of the airports are defined by the total scheduled seats of

the MAS at Q3, 2019.

Figure 3: The distribution of OD HHI in top 29 MASs before (Q3 2019)

and during late stage of pandemic (Q3 2022) (other than top 5

MASs)Figure 4: The Average OD level HHI for top 30 MASs before (Q3 2019)

and during late stage of pandemic (Q3 2022) (other than top 5

MASs)

Table 10: Airline HHI of MASs before (Q3 2019) and during late stage of

pandemic (Q3 2022) (other than top 10 MASs)

Rank

MAS

Region

Before

Late stage

Diff%

11

Moscow

Europe

0.205

0.2

-3%

12

Dubai

Latin America & Middle East

0.372

0.282

-24%

13

Seoul

Asia-Pacific

0.119

0.126

6%

14

Dallas

North America

0.504

0.491

-2%

15

San Francisco

North America

0.18

0.196