Solving the mystery of discrepancies and double counting in air cargo through demand and supply big data analysis

Vincent Van Bockstaele[1], Sven Buyle[1] and Wouter Dewulf[1] [1]Department of Transport and Regional Economics, University of

Antwerp, 2000 Antwerp, Belgium

Abstract: This paper estimates and analyses the air cargo

demand and supply imbalances between large geographical regions based on

newly collected demand and supply data. Due to the need for more data

for academics and the industry, and the lesser research interest

compared to its passenger counterpart, limited empirical research on air

cargo market dynamics has been conducted. Live flight and aircraft data

were collected for five consecutive years to reconstruct the air cargo

network and capacity. Air cargo sales tonnes data were collected and

introduced as these data eliminate double counting of transfer route

volumes. Both datasets were used and compared to analyse the air cargo

trade imbalances. The major findings indicate an imbalance in demand on

most of the 110 studied region pair combinations. The supply data

indicate a high imbalance for freighter capacity, a relatively smaller

imbalance for integrator capacity and a limited imbalance for the

wide-body belly capacity. The data indicate that the Middle East,

Northeast Asia, Russia, Central Asia, and Central America regions are

all transfer or in-transit regions where a large amount of cargo passes

through. However, limited cargo volumes originate or find their final

destination here. Although the general assumption indicates that air

cargo supply follows air cargo demand, imbalances between demand and

supply in opposing directions were found for several region pairs. To

the best of our knowledge, this paper is one of the first academic

sources to introduce data analysis based on sales tonnes. This research

assists academics and the industry in getting a better understanding of

the current air cargo market dynamics. It also provides a base to

enhance future air cargo market research, analysis and forecasting.

Keywords:Air cargo demand and supply imbalances;Sales tonnes demand data;Air cargo market analysis Citation:Van Bockstaele, V., Buyle, S., and Dewulf, W. (2023). Solving the mystery of discrepancies and double counting in air cargo through demand and supply big data analysis. Journal of the Air Transport Research Society 1(1): 81-100 DOI:https://dx.doi.org/10.59521/6A961EF46EB809C5 Download:PDF

1 Introduction

With 60.9 million tonnes of goods transported in 2021, less than 1%

of world tonnes are estimated to be carried by air cargo. Because of the

high value of these goods, they represent about 35% of the value of

goods shipped globally (Boeing, 2022). The increase in air cargo rates

to record-breaking levels attracted much interest from inside and

outside the industry. Other than the bi-directional nature of air

passenger flows, air cargo tends to move from manufacturing to

distribution centres or from production to consumption centres causing

imbalances in air cargo flows (Zhang and Zhang, 2002). Those imbalances

are especially important for the planning departments of airlines

operating freighter aircraft as those aircraft often perform triangular

or multisector routes to cope with those imbalances (Bombelli et al.,

2020). Another way airlines cope with air cargo demand imbalances is by

applying a hub and spoke network. By using a hub and spoke system,

airlines can consolidate air cargo flows in their hub to optimise their

capacity and increase their revenues. Although air cargo was considered

a by-product for passenger airlines in the past, the COVID-19 pandemic

made those airlines rethink their cargo activities to survive. One of

the main problems in air cargo research is the shortage of publicly

available air cargo data. Although some data published in reports by

major institutions like IATA1, ICAO2 or

Boeing3 are available, their data are

generally published on an aggregated market or region level. Although

comprehensive disaggregated data is often published by organisations

like EUROSTAT or the US Bureau of Transport Statistics for a certain

region, collecting disaggregated data for other regions or combining

those datasets to build a comprehensive dataset comprising all regions

and countries can be rather time-consuming.

This papers comprehensive actual flow database is constructed through

intensive data collection. Flight data from three main flight-tracking

websites were collected, cleaned and combined into a database. The

database consists of data from January 2018 until December 2022.

Although data from flight tracking websites were already sources in

previous research (Bombelli, 2020; Bombelli et al., 2020; Malighetti et

al., 2019a and 2019b), it will be the first time data from three

different sources and over five years were collected and combined.

Combining heterogeneous datasets can be a rather tedious task as it

might cause challenges. The main challenges found were the different

features published by the different sources, time zone deviations,

mismatches in departing and arrival timings, and missing data. We

addressed those problems by working with features that were available

for all rows, transferring all rows to the same time zone, working with

time buckets, and removing rows that were not useful due to the missing

data. Afterwards, we compared the Available Cargo Tonnes (ACT) of 2021

of our comprehensive database with the ACT numbers IATA published. Next

to introducing a comprehensive flight database, we also introduce, to

the best of our knowledge, the first international sales tonnes data

into the academic literature. Sales tonnes data are the actual tonnes

sold and transported by air without double counting due to transfers or

in transit. Both datasets were used to estimate the air cargo demand and

supply on industry and region-to-region levels. Different types of data

originating from different sources are compared to indicate the

importance of understanding which data types are used. After providing a

market overview of air cargo demand, supply, and rates, a

region-to-region analysis for the 2022 data is conducted to estimate the

amplitude of the air cargo sales tonnes flows and imbalances between

different regions. The same analysis is conducted for the supply side

for wide- body belly capacity, dedicated freighter capacity and

integrator capacity.

The rest of the paper is organised as follows. Section 2 provides an overview of the

current air cargo demand studies, supply studies, and data sources used

in the academic research. Section 3 presents the

methodology and data collection process. Section 4 gives an

overview of both air cargo demand and air cargo supply on an aggregate

level and discusses data problems of different sources and problems when

comparing different sources. Section 5

focuses on the air cargo demand and supply imbalances separately and

compares both imbalances. Section 6 provides conclusions,

limitations and recommendations for future work.

2 Literature review

Although air cargo studies are generally considered underrepresented

in the academic literature compared to their passenger counterparts, air

cargo research has received growing interest in the last fifteen years.

Air cargo studies can be classified into four broad categories (Yu and

Zou, 2022); (1) competition and connectivity of airports in the air

cargo market, (2) air cargo market structure and airline competition,

(3) air cargo operations, and (4) analysis and estimation of air cargo

demand and its relationship with economic or trade growth. This research

will focus on the second aspect, particularly the air cargo market

structure, and on the fourth aspect, the analysis of air cargo demand.

Of the main aspects that will be analysed in this paper, air cargo

demand is the most extensively discussed in the current literature.

2.1 Air cargo demand

While there is a general agreement that air cargo transport, as cargo

transport in general, is the result of economic activity and, therefore,

an operationally derived demand (Rodrigue, 2006; Kupfer et al., 2017),

there are some discrepancies in how air cargo demand is derived. Grin

(1998) discusses that air cargo demand can usually be seen as a derivate

of transport, which in itself is a derivate of trade. Meanwhile,

Holloway (2008) states that air cargo depends on the underlying demand

for goods requiring rapid transportation as well as on the costs and

benefits of air cargo compared to alternative modes of transportation.

Those discrepancies are present in defining how air demand can be

derived and determining the underlying parameters for air cargo

forecasting. Most air cargo demand studies focus on the relationship

between air cargo and economic growth (Alici and Akar, 2020). The Gross

Domestic Product (GDP), an indicator of economic development, is one of

the most studied determinants for air cargo by academic researchers.

Kasarda and Green (2005) study the empirical relationships between air

cargo, trade, and GDP per capita to quantify air cargos role in economic

development. Wadud (2013) simultaneously forecasted demand for passenger

and cargo at the Shahjalal International Airport using GDP, national

price levels, and oil prices as determinants for the demand. Morrell and

Klein (2018) identified GDP, international trade, oil prices, exchange

rates, interest rates, and globalisation as key variables for

forecasting future air cargo demand.

Although GDP is a good indicator of the growth and health of an

economy, the role of GDP in air cargo demand forecasting can be

questioned (Kupfer et al., 2011). Last decades the development of the

importance of services in GDP caused the relationship between GDP and

air cargo to become less straightforward. While services made up 53% of

the world GDP in 1970, this number increased to 64.4% in 2021.

High-income countries generally have a higher share of services in their

GDP, for example, a share of 71.8% in high-income countries versus 39.1%

in low-income countries (Worldbank, 2022). As a result, global value

added is increasingly being generated by services rather than economic

activities that may generate air cargo. Kupfer et al. (2017) propose to

use merchandise trade and share of manufactures in merchandise trade

instead of GDP and industrial production, which is often used to

represent the link between economic activity and transport and can also

be considered a weak indicator for air cargo. Other authors (Hamal,

2013; Lakew and Tok, 2015; and Alexander and Merkert, 2021) also

forecasted air cargo demand at airport, regional, and country levels

without using GDP as an indicator.

Boeing (2022) states that although air cargo accounts for less than

1% of the world’s trade tonnes, it is responsible for about 35% of the

value of all globally shipped goods, indicating the high value of these

goods. Air cargo commodities can be classified in different ways and

product types based. The IATA classification, which divides air cargo

into general and special cargo, is widely used in the industry. Special

cargo are goods that, due to their nature, weight, dimensions, and/or

value, may have specific requirements, including packaging, labelling,

documentation, and handling through the transport chain. The transport

of those goods is addressed through specific regulations that must be

followed when preparing, offering, accepting, and handling this cargo

(IATA, 2023). Special cargo is subdivided into the following products;

valuable, pharmaceuticals and temperature-controlled, live animal,

vulnerable, dangerous, and perishables products. One of the

classifications flaws is the large allocation to general cargo. Another

classification for air cargo commodities was made by Doganis (2010),

classifying air cargo into manufacturing goods, machinery and transport

equipment, and a remaining part consisting of a variety of different

commodities, among which fresh foods, medical and pharmaceutical goods,

as well as chemicals, are of particular importance. Each of the three

classes comprises one-third of the worldwide air cargo tonnes. In

addition to those two classifications, each countrys statistical and

data embodiments have their classification of air cargo products, making

data source comparison difficult. Many authors (Holloway, 2008; Doganis,

2010; Shaw, 2016) prefer to segment the air cargo market based on the

shipper’s motivation and journey urgency rather than considering

individual commodities. They identified four key commodity types in

increasing order of price sensitivity: emerging freight, high-value

freight, routine perishables freight, and routine non-perishable

freight. Whatever classification system is used, there are differences

in air cargo flows when comparing regions, countries, and airports, as

indicated by Boeing’s world air cargo market forecast.

According to Zhang and Zhang (2002), economic activity in the

importing region drives cargo movement from manufacturing to

distribution centres or from production to consumption centres.

Different levels of commercial activity at either end of a route can

amplify directional imbalances in cargo tonnes, and commodities carried,

mainly if the two points are at different stages of the economic cycle

(Holloway, 2008). This effect of the economic activity in the importing

region and the various stages of the economic cycle also explains the

different types of products transported by air on a region, country, and

route level. On the Europe-East Asia route, for example, 27% of cargo on

the East Asia-Europe leg consists of computers, office, communications,

and professional equipment. In comparison, those goods represent only 8%

of the air cargo flown on the Europe to East Asia leg. Both Boeing

(2022) and Morrell and Klein (2018) provide an overview of the main

imbalances in air cargo demand. The data they used is actual tonnes

carried data and includes transfer and in-transit data. By including

this data type, they analyse the imbalanced carried flows rather than

the actual import and export imbalance between regions.

2.2 Air cargo supply

Airlines have different strategies when it comes to cargo operations.

Generally, airlines handling cargo can be divided into integrators,

freighter carriers, combination carriers, and passenger carriers (Li et

al., 2012). Integrators (e.g., DHL, UPS, and FedEx) sell capacity to

shippers directly through direct market channeling. Through indirect

market channeling, they sell their excess capacity to freight

forwarders. Freighter carriers are airlines dedicated to transporting

air cargo (e.g., Cargolux). Those airlines only operate dedicated

freighter aircraft and sell their capacity through indirect market

channeling. Combination carriers only transport cargo with passenger

aircraft (e.g., British Airways) or with both passenger and dedicated

freighters aircraft (e.g., Lufthansa). Passenger airlines focus on

passenger operations and do not transport cargo (e.g., Ryanair). (Feng

et al., 2015). Historically, air cargo was considered a by-product of

passenger transport. In the last twenty years, many traditional carriers

have considered it an instrument for profit maximisation (Kupfer et al.,

2012). Focusing simultaneously on cargo and passengers can enable

multiple benefits for passenger carriers (Gangwani, 2015). Air cargo

allows passenger carriers to offer routes that are not commercially

viable on passenger demand alone but also enables them to offer higher

frequencies on their existing routes. Due to the marginal costs of

transporting cargo into the belly hold of passenger aircraft, carriers

can increase and diversify their revenue streams and margin per

route.

Cargo can be transported on different types of aircraft. The most

common breakdown in academic literature divides aircraft into passenger,

freighter, combi, and convertible aircraft. Most aircraft are passenger

aircraft transporting passengers on the main deck and luggage and cargo

on the lower deck. Freighter aircraft only transport cargo and can be

either dedicated or converted. Dedicated freighters are aircraft

designed from the beginning only to transport cargo, while converted

freighters are passenger aircraft converted to freighter aircraft. Due

to previous passenger requirements, the last type has some payload

restrictions that dedicated freighters do not have. Convertible aircraft

are limitedly built and can switch the number of seats on the main deck

to allow more or less cargo payload. Although those aircraft were famous

in the past, today, they can be considered neglectable due to the

minimal number of those aircraft in the overall fleet. In the academic

literature, the focus can be on all aircraft types (Kupfer et al., 2011;

Morrell and Klein, 2018; Bombelli et al., 2020), freighter aircraft

(Budd and Ison, 2017), or passenger aircraft (Merket and Ploix,

2014).

Both passenger and freighter aircraft have their benefits and

limitations. First, freighters are generally used in markets with higher

demand for cargo than passengers and markets with an imbalance between

incoming and outgoing cargo (Kupfer et al., 2011). Second, freighter

aircraft are used to transport cargo that, due to its dimensions or

hazardous characteristics, is not suitable to be transported in

passenger aircraft (Merket and Ploix, 2014). Although there is a market

for hazardous and oversized cargo, only 5 to 15% of all air cargo is

bounded to be transported on freighter aircraft (Boos, 2015). Third,

freighter aircraft are particularly well suited for transporting

high-value goods because they provide highly controlled transport,

direct routing, reliability, and unique capacity considerations (Boeing,

2017). Last, the capacity of freighter aircraft is fixed, which is

different for belly capacity with a varying capacity to short-term

variations in passenger numbers and luggage weight and sizes (Amaruchkul

et al. 2010). This guaranteed capacity offers airlines and consignors

better flown-as- booked rates (Crabtree, 2014). The belly capacity of

passenger aircraft is smaller than the cargo capacity of freighter

aircraft. Therefore, the marginal costs of filling up this capacity are

generally only one-third of the cost of filling up a freighter capacity

(Morrell and Klein, 2018). The lower marginal costs make belly capacity

particularly suitable for air cargo products with lower yields, like

some types of perishables and general cargo.

In the last couple of years before the COVID-19 pandemic, around half

of the air cargo was transported on freighter aircraft, and the other

half was transported as belly cargo on passenger aircraft. As discussed

in the previous section, different levels of commercial activity at

either end of a route can amplify directional imbalances in cargo

tonnes. This uneven spatial nature of air cargo demand is often referred

to as the backhaul problem (Budd and Ison, 2017). Although the backhaul

problem causes airlines to struggle with finding enough volume to fill

their capacity on some legs, airlines operating freighters often fly

triangular and multisector routes to cope with this problem. Bombelli et

al. (2020) presented a complex network analysis of the air transport

network using the air cargo perspective. They found that the percentages

of origin-destination airport pairs served in both directions and in a

single direction are 77 and 23%, respectively. Because of the

bi-directional nature of passenger traffic, belly capacity is bound to

fly both legs of the same route, making the backhaul problem even more

significant for belly capacity. Due to the backhaul problem, the higher

capacity uncertainty of belly capacity, and the passengers’ luggage, air

cargo weight load factors are lower on belly capacity than on freighter

capacity (Morrell and Klein, 2018). Following IATA (2021), the all-cargo

flight freight load factor was around 65%, while the mixed flight

freight load factor was around 36%. Regarding integrator network

analysis, Bombelli (2020) found very imbalanced air cargo flows for

FedEx and UPS towards their hubs in MEM and SDF, and more balanced flows

for the DHL network from November 2019 till June 2020.

Another way airlines, and especially Middle Eastern Carriers, cope

with the backhaul problem is to employ a hub and spoke network using

their strategically located hub to feed and defeed freighter and belly

capacity (Budd and Ison, 2017). Hubs are even more critical for air

cargo than for air passengers. While the top ten passenger hubs account

for only one-third of global passenger traffic, the top ten cargo hubs

account for two-thirds of global freight traffic (Holloway, 2008).

Integrators atypically operate from a hub and spoke network in North

America, but Malighetti et al. (2019b) also found hub and spoke networks

for the European market. Malighetti et al. (2019a) studied the air

transport networks of global integrators in the more liberalised Asian

air cargo industry and found that integrators operate extensive multi-

hub networks in the Asian market as well. Air cargo has a much larger

catchment area than the air passenger side. The larger catchment area

allows airlines to feeder their flight by trucking. Especially in

Europe, where trucking distances are relatively small and good

infrastructure is present, trucking is common. Although it is common,

Baier et al. (2021) argue that a quantitative approach to automate a

clear-cut catchment area of airports for air cargo is complex due to the

unprecise trucking networks processing airfreight from and to airports.

Although freighter aircraft carry around half of the total air cargo,

their role has often been questioned and examined. Following the

financial crisis in 2008/2009, there was overcapacity in the market,

causing airlines to ground and retire freighter aircraft. In times of

crisis and overcapacity, airlines switch from freighter aircraft to

belly-capacity aircraft (Kupfer et al., 2017). The overcapacity was

present due to the economic downfall causing lower air cargo volumes to

be transported, new passenger aircraft with higher belly hold capacity,

a modal shift towards cheaper sea shipping, and an increase in

international trade protection measures restricting cross-border trade

(Budd and Ison, 2017). Although new aircraft have higher payloads for

air cargo due to increased size and fuel efficiency gains, their impact

on overcapacity is not yet significant (Boeing, 2017). Although the

general grounding and retirement of freighters in this period, in some

world regions, the demand for freighters kept growing (Budd and Ison,

2017). In times of crisis and overcapacity, airlines switch from

freighter aircraft to belly-capacity aircraft. Although many freighter

aircraft were not expected to have a future any longer, the COVID-19

pandemic caused freighter aircraft to be a crucial asset in transporting

air cargo. Ageing cargo aircraft were being taken out of storage and

returned to service (Macário and Van de Voorde, 2022).

2.3 Air cargo data sources

Publicly available air cargo data for academic purposes are scarce.

One of the reasons for this scarcity can be found in the confidentiality

of the data and the competition for the data (Bombelli et al. 2020). The

problem is even more severe when it comes to integrator data (Lakew,

2014 and Malighetti et al., 2019a). Gong et al. (2017) claim that the

shortage of comprehensive data on price and traffic volumes at the route

or airline level is one of the main reasons air cargo is lesser

developed than its passenger counterpart. This conclusion was also found

by Wei (2006), who indicated that the unavailability of sufficient,

accurate and consistent data in the air cargo industry is one of the

reasons for the lack of in-depth air cargo research. Although there is a

scarcity of publicly available aviation market data for academic

research, some nuances can be made.

First, large institutions and companies like IATA, Boeing, and the

ICAO often collect and make publicly aggregated market data available.

IATA publishes the IATA World Air Transport Statistics (2021) on a

yearly level providing information on air cargo demand, capacity and

payload levels. One of the shortcomings of this database, other than the

unavailability of public access, is the level of aggregation of the

data. Although a distinction is made between international, domestic,

scheduled, charter, and all cargo flights, the data is aggregated per

airline per year. This makes the data suitable for more aggregated

research but less suitable for more disaggregated analyses, especially

for origin-destination research. Publicly available air cargo data for

those three sources do not come in the form of datasets but can rather

be found in reports. One of those reports is the monthly Air Cargo

Market Analysis from IATA (2014-2023). Those monthly reports provide an

update on the current situation of the air cargo market and data on air

cargo demand and supply on an international and main region level. One

of the shortcomings of the data is that those reports often publish

percentage change data rather than absolute numbers. However, some

reports also include actual numbers, which makes it possible to use

those percentages to estimate the missing absolute numbers. The same can

be done for IATA’s quarterly Air Transport Chartbook reports (IATA,

2015-2023) and for ICAO’s Annual Reports of the Council (ICAO,

2008-2021). Next to the time-intensive task of analysing all those

reports, the methodology of how the data behind those reports are

collected is often unclear. Next to both sources, Boeing publishes its

bi-annual World Air Cargo Forecast and its commercial market outlooks

(Boeing, 2022). Because only the latest report is published on the

Boeing website, older reports are often more difficult to obtain. Unlike

the IATA and ICAO reports, Boeing published more absolute figures in its

report making the reports more convenient to use. However, much detailed

or older data is still hidden in graphs and percentages, which can be a

shortcoming if you are looking for those specific data.

Second, disaggregated data is also often available, but the task of

collection and cleaning is time-consuming. Disaggregated air cargo

demand data is often published in countries’ databases and can be

accessed through a web portal or an application programming interface

(API). Although looking for the data is not necessarily time-consuming,

cleaning the data due to inconsistencies between sources, methodologies,

data types, and data features is. Disaggregated air cargo supply data is

often more hidden than its demand counterpart. Wei (2006) discussed that

the problem of inconsistencies between disaggregated data sources and

not knowing which data source is the most accurate or consistent is one

of the main problems in air cargo data. Wei (2006) explored the

available data sources and databases related to air cargo studies to

investigate what data are available and what analysis can be made based

on current data sources to study air cargo activity at a state level,

specifically in California. Eight major, mainly North American data

sources were studied and explained. He found that the data of those

sources either came from airlines, airports, or shippers who each report

data collected from their own perspective. The airline data mainly

originates from the US Bureau of Transportation Statistics (BTS) who

collects and compile data from certified air carriers on Schedules T-100

and T-3. Airport data is mainly published by airports themselves and by

the Airport Council International (ACI), who publishes the Annual

Worldwide Airport Traffic Report based on a survey of large airports

worldwide. The last type of data, originating from shippers and

logistics companies, is obtained by the Commodity Flow Survey (CFS). CFS

is a survey of shipments by domestic establishments in manufacturing,

wholesale, mining and selected other industries. Because all sources

collect data considering their own perspectives, it is not surprising

that the published data of the above sources are inconsistent. A second

problem between those databases is that some important features are

missing, such as the value of the goods transported, the routing of the

goods, the production location, the final destination, etc. The last

problem is with the CFS database. Although Wei (2006) considered the CFS

database to be the most ‘useful’ as the database classifies the data of

the flow of types of goods and materials by mode of transport, the

database is not published yearly. The latest publication that could be

found was of 2017.

Table 1 provides an overview of large data sources used in the

academic literature. With large data sources, we refer to sources that

cover the whole world, like the Official Aviation Guide (OAG) database

or the Airport Council International (ACI) database, or data sources

that cover a large region, like the US Bureau of Transportation

Statistics (BTS) or Eurostat, the database of the European Union and its

partnering countries. Datasets only covering large regions of certain

continents, like BTS or Eurostat, are often used to conduct case studies

or to analyse certain routes, regions, or sub-regions (Bowen, 2012 and

Morrell and Klein, 2019). Bowen (2012) used the BTS data of 2010 to

assess the network evolution of both FedEx and UPS. Although the

database is relatively complete, he argued that one of the shortcomings

was that there was no data on integrators’ traffic carried on partner

airlines which could slightly affect their results. A database used in

air cargo tis the OAG database. The OAG database consists of historical

published flight schedules, excluding actual non-scheduled flights and

non-IATA members’ flights (Heinits and Meincke, 2013). Although charter

flight takes up around 5% of the international air cargo capacity

(Boeing, 2009-2021), the impact of the missing charter data in the OAG S

is yet unsure. The problem of missing charter and non-scheduled flights

is not only a shortcoming of the OAG but also of the Seabury Consulting

dataset. Bombelliet al. (2020) discussed that the Seabury Consulting

dataset was missing integrator, LATAM, charter and other non-scheduled

flights. The dataset they received from Seabury Consulting contained

origin-destination data for 2014. They collected the missing data to

fill the gap using the flight tracking website FlightRadar24. Although

flight tracking websites have been around for quite some time, it is

only recently that authors like Malighetti et al. (2019a and 2019b),

Bombelli et at. (2020) and Bombelli (2020) started collecting actual

flight data for air cargo purposes, mainly network analyses. Although

those types of data can be very useful for analysing market dynamics,

competition analyses, route scheduling problems etc. as they are very

disaggregated, the collection of such data is highly time-consuming as

the data is often only available for one week.

Table 1: Major air cargo data sources used in publications.

Reference

Objective

Data Source

Description

Constraints

Bowen (2012)

Assessment of the network evolution of

FedEx and UPS

US Bureau of Transportation Statistics

(BTS)

Monthly reported domestic and

international airline data for certified U.S. air carriers and data of

foreign carriers having at least one service point in the United States

or its territories. Data for 2010.

No data are recorded for sectors that

begin and end outside the US. No data on integrator traffic carried on

partner airlines.

Heinitz and Meincke (2013)

Construct a multistep, twofold

capacity-restrained itinerary-based demand assignment algorithm.

Official Aviation Guide (OAG)

Published recent and historically

scheduled flights. Sample data for a week in 2007.

The dataset excludes the actual

non-scheduled flights and flights of non-IATA airlines, such as

integrators.

Song and Yeo (2017)

Analysis of the air transport network

using the social network analysis approach.

Airport Council International (ACI)

Data on the top 20 airports in 2016 based

on passenger, cargo, and movements.

No data is publicly available outside the

top 20.

Song and Yeo (2017)

Analysis of the air transport network

using the social network analysis approach.

Web pages of airlines alliances

Reconstruction of the route network in

March 2017, taking into account 1,060 airports in 173 countries. In

total, 5,580 routes were constructed.

Exclusion of non-alliance members. Focus

on international rather than domestic routes.

Morrell and Klein (2019)

Providing an overview and status of the

air cargo industry

Eurostat

Overview of traffic between

origin-destination airports where at least one airport is located in the

European Union or one of the partnering countries. Overview of data from

2006 until 2016.

None

Morrell and Klein (2019)

Providing an overview and status of the

air cargo industry

BTS

See Bowen (2012). Data for 2015.

See Bowen (2012)

Morrell and Klein (2019)

Providing an overview and status of the

air cargo industry

Boeing WACF

Overview of aggregated air cargo flows

between pre-defined major regions based on 2015 data.

Data is only available for the major

region pairs, neglecting smaller air cargo flows.

Morrell and Klein (2019)

Providing an overview and status of the

air cargo industry

IATA WATS

Overview of aggregated air cargo carried

per airline in 2016.

Data is not publicly available

Malighetti et al. (2019a)

Analysis of the Asian air integrator

networks by graphical analysis and complex network metrics.

FlightRadar24

Data on flights “departing from” and/or

“arriving at” one of the airports located in Asia. Sample data for one

week in 2015.

Not possible to investigate a temporal

evolution of the network since the data set merely provides a picture of

the networks’ structures.

Malighetti et al. (2019b)

Network analysis of the integrators in

Europe

FlightRadar24

See Malighetti et al. (2019a)

See Malighetti et al. (2019a)

Bombelli et al. (2020)

Complex network analysis of the air

transport network using the air cargo perspective

Seabury Consulting flight schedule

database

List of airports characterised by a yearly

international cargo throughput of 5,000 tonnes or higher + the yearly

frequency per aircraft type for all OD airport pairs. Dataset was based

on 2014 data.

Integrator, LATAM Cargo, narrow body

passenger, charter and other non-scheduled operation data excluded

Bombelli et al. (2020)

Complex network analysis of the air

transport network using the air cargo perspective

FlightAware

All recorded departures were collected for

each airport part of the air cargo transport network. Data was collected

from June 2019 until January 2020.

Only data for seven months due to time

limitation

Bombelli (2020)

Analysis of the global networks of

integrators using network science

Flightradar24 and FlightAware

Pre-selected a set of 336 airports deemed

relevant from a cargo perspective (i.e., with an annual cargo throughput

in 2014 greater or equal to 5000 tonnes. Data were collected from

November 2019 until June 2020.

Ruling out lower-tier airports Temporal

holes due to not starting the data retrieval process at the correct

time

Due to the time intensity of the data collection, the authors only

collected the data from one week to a few months. Although taking

samples might be interesting to get a picture of a certain moment in

time, it would be more interesting to analyse market dynamics to better

understand those pictures evolution. Although this paragraph provides a

basic overview of data sources used in air cargo research, there is a

need for more in-depth analyses of air cargo sources to understand their

benefits and shortcomings. Next to understanding those data sources and

their differences, there is also a need to find or construct a benchmark

database against which other sources can be compared.

2.4 Summary and contribution

In summary, the current academic research on air cargo market

dynamics needs to be enhanced. Although some research has already been

conducted on air cargo demand and supply separately, much research is

yet to be done on a combined analysis of both demand and supply. One of

the main problems in the current literature regarding air cargo is the

need for more comprehensive data, which is required to perform more

in-depth analyses to better understand air cargo market dynamics. The

contribution of this paper is twofold: (1) New air cargo demand and

supply data is collected from various sources and combined into one

comprehensive dataset. (2) The dataset is used to analyse both air cargo

demand and supply imbalances on a region-to-region level separately and

simultaneously.

3 Methodology and data

description

3.1 Methodology

This research uses an inductive approach to conduct an air cargo

data-driven market analysis on the global market and the main trade

lines. Air cargo-related market data on the network, demand, supply, and

aircraft will be sourced from multiple sources on a disaggregated market

level. The data will be jointly analysed to provide an overview of the

air cargo market and identify patterns and relations. The inductive

approach is chosen for two reasons. First, air cargo market research is

scarce, and few theories have yet to be developed. The inductive

approach allows us to start with market observations and develop new

theories and insides through analysis and pattern recognition to fill

this gap in the current literature. Second, the air cargo market is

complex, with different sub-market characteristics. The inductive

approach allows us to start with disaggregated data to better understand

those complex dynamics before going to a more aggregated level.

3.2 Data

The air cargo data collection for this research was carried out over

one year, where data from different sources between 2018 and 2022 were

collected. First, aircraft data was sourced from Airfleets4 and

PlaneSpotter5. Both sources provide information

about aircraft movements between operators and provide an overview of

the status of airframes for all airlines worldwide. The registration

plate data for all wide-body and narrow-body freighter aircraft between

2018 and 2022 were collected. This way, the actual and historical

registration plates for the aircraft were included. The collected

wide-body registration plate data was used as input on flight tracking

websites to collect flight data. Three flight tracking websites were

considered: Flightera6, Flightradar247 and

FlightAware8. All have published flight data on

flight date, origin, destination, actual departure time, arrival time

and flight duration for each registration plate. Flightera and

Flightradar24 also provide data on the flight number. Data from

Flightera is freely available for December 2017 onwards and was

collected from January 2018 until February 2022. Flightradar24 data was

collected from October 2019 to December 2022. FlightAware data was

collected from October 2021 until December 2022. Due to resource

constraints, mainly time constraints as collecting such an amount of

data can be rather time intensive, the narrow-body freighter data was

only collected from FlightAware and Flightradar24 for 2022. All the

collected data were combined. Combining heterogeneous datasets can be a

rather tedious task as it might cause challenges and problems. Next to

differences in features published or missing data, dealing with near

duplicates due to time zone differences or time deviations were also

major challenges. Those four challenges were solved as follows:

When comparing and integrating those sources, the first challenge

tackled was the mismatch of features between the different flight

tracking websites. All sources published data on the day, month and year

of the flight, the origin and destination, and the departing and

arriving times. Due to the scope of this research, those features were

sufficient, and all the others were removed. Although those features are

sufficient for the purpose of this research, flight code or scheduled

departure and arrival times might be interesting for future research.

The flight codes can be interesting in identifying the code-sharing

behaviour of airlines, analyses of individual airline networks or

calculation of market shares on certain routes and networks. Scheduled

departure and arrival times can be interesting for airport analyses,

airline punctuality, or for research towards airport optimisation

models.

The time-zone problem was solved by converting all times to the

Coordinated Universal Time (UTC).

The small mismatches in timings were partly solved by counting

the flights with the same data, origin, destination, and registration

plate per source. First, if there were no duplicates, we assumed that

there was only one flight with that specific aircraft between the origin

and destination on that day. The results for all three sources were

compared, and the timings were considered if the flight had no

duplicates in all sources. If the differences between the UTC timings

between all three sources were less than 15 minutes, we assumed those

flights to be duplicates. The decision must be taken manually if the

difference was higher than 15 minutes, which was rarely the case.

Second, if duplicates were found or some sources found a duplicate while

the others did not, time brackets of one hour were used, meaning that

each timing was rounded to the closed hour. Afterwards, the process was

repeated, including the new time brackets. If there were still problems,

those cases also needed to be checked manually. We are aware that this

probably does not solve all mismatched timing and that one of the two

can be rounded off to the previous hour while the other can be rounded

off to the next hour. Although we acknowledge that our methods of

dealing with mismatches in timings are not perfect, we believe the

overall impact to be limited.

Regarding the missing data features, the main missing features

were origin or destination related. As filling in the missing data was

impossible, those rows were removed.

Afterwards, we compared the Available Cargo Tonnes (ACT) of 2021 with

a correction of the narrow body freighter capacity of 2022, as we do not

have them for 2021, of our comprehensive database with the ACT numbers

published by IATA in its quarterly chartbooks (2015-2023). We found our

ACT data to be 6.3% above that of IATA. Although the 6.3% may indicate

that not all duplicates were removed, we believe the maximum payload for

each aircraft used can explain the difference. Because the maximum

payload is seldom reached, our data is subject to overcalculation which

might explain the 6.3%. Because we are aware that our methods are not

perfect, we believe more research is required on the integration of

different sources, the payloads used, and the comparison of our dataset

with more data sources to validate our methods.

Combining those three sources allows for a more comprehensive

database. The combined database is then compared to the three sources

individually to assess the accuracy of each source. Flightradar24 was

the most comprehensive source covering 91% of the combined database.

FlightAware covers 88%, and Flightera 83%. As Flightera is our prime

source for January 2018 until September 2019, a deeper dive into the

data was conducted to understand better which data is missing leading to

an 83% accuracy. As it turns out, wide-body passenger aircraft flights

have an accuracy of 96%, even higher than the Flightradar24 data. The

problem is with the full freighter data. By analysing the freighter data

on a daily level, a steep decline of 50% of data is found in July 2019.

Extra freighter data from May 2019 until September 2019 was collected

from Flightradar24 to determine if the decline is due to data issues or

sudden events in the market. As the Flightradar24 data does not show any

decline, we concluded that the Flightera data has a gap in freighter

data from July 2019 onwards. This gap was filled by including the extra

Flightradar24 data. The combined database was cleaned by combining the

origin and destination IATA codes with their respective countries,

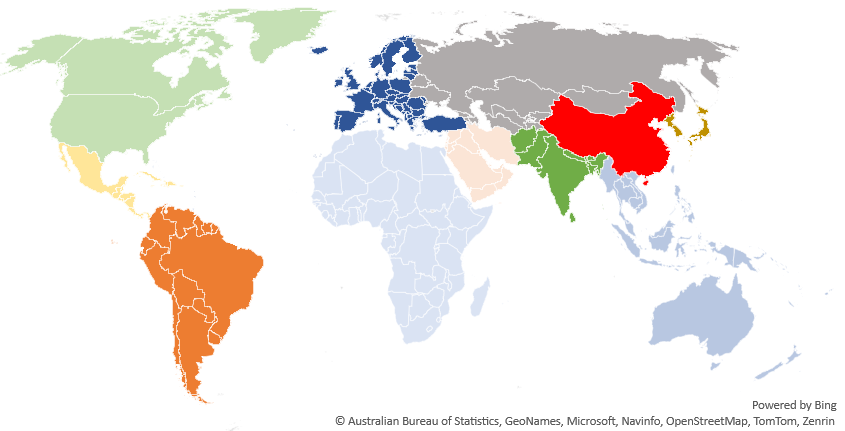

regions, and coordinates. The regions are defined as shown in Figure 1;

North America (NA), Central America (CA), South America (SA), Europe

(EU), Africa (AF), Middle East (ME), Russia and Central Asia (RU),

Northeast Asia (NEA), Southeast Asia (SEA), China (CH), and Indian Sub-

Continent (INS). The available maximal payload was applied for each

flight based on the cargo tonnes for different aircraft types defined by

Bombelli et al. (2020). For the missing aircraft types, the A350-900,

the A350-1000 and the B787-10, a payload of respectively 17 tonnes, 25

tonnes, and 13 tonnes was applied (IAG, 2023). Each flight was given an

identifier to allocate capacity to wide-body, freighter or integrator

aircraft.

Figure 1: Region definition.

The demand data originates from the World Air Cargo Database

(World_ACD). The World_ACD collects and combines Air waybill (AWB) data

to build a comprehensive air cargo market database. This database

provides sales tonnes, expressed in both chargeable and actual weights,

data from an origin airport or city to its final airport or city. The

sales tonnes data includes charters-on-AWB data and mail-on-AWB data but

excludes express flown by integrators and charter and mail data not sold

on AWBs. Chargeable weight can be defined as the measurement used by

cargo carriers to determine the price for the shipment of your goods. It

can either be the gross weight or the shipment’s volumetric weight (Chao

and Li, 2017). The data is provided for the period 2018 until 2022 and

is provided on a country-to-country level. The country-to-country data

are transferred to region-to-region data based on previously defined

regions. The data also includes trucking on AWB data, but we believe the

impact will be limited due to the aggregation of the data to regional

levels. Next to the World_ACD data, demand and supply data was collected

from IATA’s quarterly published air cargo chartbook as well as from

IATA’s monthly published air cargo analysis. Next to IATA, data are also

sources from Boeings’ world air cargo forecast published bi-annually and

from ICAO’s annual report of the council.

4 Aggregated global market

analysis

This section will discuss air cargo demand and supply based on

aggregated global market data. Different types of air cargo demand data

sources are compared and discussed. Afterwards, the role and impact of

double counting due to transfer data are explained. Regarding the air

cargo demand, the air cargo capacity is estimated and allocated to

wide-body belly capacity, freighter capacity, and integrator capacity.

Finally, both air cargo demand and supply are compared and air cargo

rates are included.

4.1 Air cargo demand

Air cargo demand data are the most readily available. The most common

unit of measurement of air cargo demand is the Freight Tonne Kilometre

(FTK), representing the transport of one tonne of freight over one

kilometre. Multiple international organisations publish air cargo demand

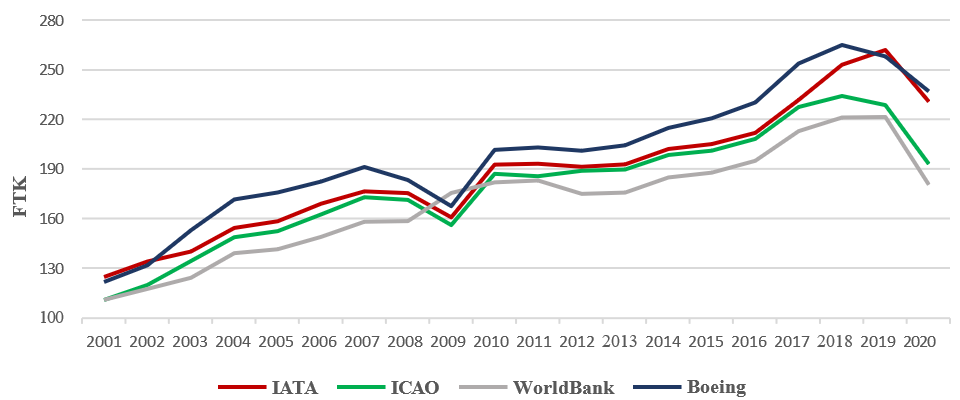

data expressed in FTK. Figure 2 shows the FTK data IATA, ICAO, the World

Bank, and Boeing9 provided from 2001 until 2020. As

Figure 2 illustrates, reported FTK data from different sources shows

discrepancies. Those discrepancies are common, as each organisation has

its methodology for collecting and defining FTK.

For 2003-2017, IATA and ICAO data are relatively similar. The

similarity is not a coincidence, as both sources publish scheduled FTK

data. Although both sources publish the same kind of FTK data, since

2018, the IATA data has suddenly increased compared to the ICAO data. In

the last few years, IATA started using Cargo Tonne Kilometres (CTK)

rather than FTK as their main reporting unit for air cargo demand. CTK

data included freight, mail, and unaccompanied baggage. Although the

data for those years was reported in FTK, we assume it is probably CTK

data as it matches other CTK data published by IATA. Unfortunately, no

confirmation by IATA could be found. The FTK data published by Boeing

are higher than IATA’s or ICAO’s figures. The difference can be found in

charter data, as Boeing issued actual rather than scheduled data. The

World Bank data, a source often used for forecasting air cargo demand,

is based on ICAO data. For most of the years, it follows the same trends

as the ICAO data, except in 2009, where it increased while all the other

sources show decreasing demand due to the financial crisis. Regarding

data usage and comparison from institutions, one must take into account

which data is included or excluded.

Figure 2: Industrys freight tonne kilometre evolution.

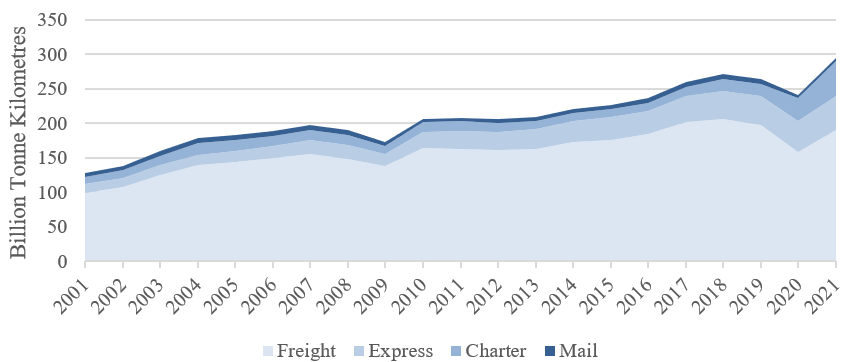

Figure 3 illustrates the global evolution of actual cargo

tonne-kilometres performed by the industry. The growth of air cargo is

similar to the growth of air freight, with a drawback in 2008 and 2009

due to the financial crisis and in 2020 due to the COVID-19 Pandemic.

The first drawback can also be found for international express cargo, as

the financial crisis impacted the purchasing power of the customers.

Compared to the second drawback of freight in 2020, express boomed by

8.1% compared to 2019. This increase can be explained due to people

spending more money on online shopping as they needed less money for

social activities and travelling due to lockdowns. International express

cargo is the quickest-growing air cargo segment growing from an

international market share of 13.4% in 2008 to 21% in 2021. Compared to

the ever-increasing express segment, the air mail segment steadily

decreased from a market share of 5.2% in 2001 to 1.8% in 2021. Although

the market share of air mail has been declining slowly over the last 20

years, the COVID-19 pandemic accelerates this decrease. Although the air

cargo charter market is a small part of the general market, with a

market share of around 6.9% before COVID-19, the COVID-19 pandemic

caused the charter market share to almost triple to 17.3% in 2021. Most

charter data is often neglected in analysing the market due to the use

of scheduled data; this increase must be addressed when observing data

from 2020 onwards. Therefore, working with actual flown data rather than

scheduled data is essential.

Figure 3: Industry’s freight, express, charter and

mail-tonne kilometre evolution.

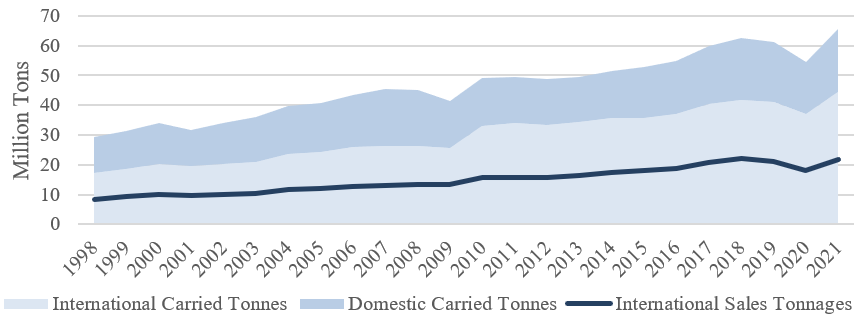

Next to FTK and CTK, another unit of measurement for air cargo demand

often used is carried tonnes. Carried tonnes express the actual weight

of all cargo transported. Figure 4 illustrates domestic and

international cargo tonnes carried from 1998 until 2021. In the first

ten years, domestic and international traffic experienced an average

growth of 4.37% per year. From the financial crisis in 2008 onwards,

international cargo traffic, with an average annual growth of 4.75%,

outperformed the 2.42% average annual growth rate of domestic

traffic.

From a financial point of view, another unit of measuring air cargo

is sales tonnes. Sales tonnes are the air cargo sold at a specific price

and transported from an origin to a final destination airport or city as

provided on the air waybill (AWB). Sales tonnes data exclude transfers,

thus excluding double counting, and are at the bases for calculating

revenue as air cargo rates are multiplied by them. Figure 4 illustrates

the international carried tonnes to be higher than the international

sales tonnes indicating much double counting into the industry. Due to

the missing express data of integrators in the World ACD data, the

international carried tonnes cannot be divided by the sales tonnes to

estimate how much double counting there is in the industry.

Figure 4: International versus Domestic carried Tonnes and

International Sales Tonnes.

4.2 Air cargo supply

Unlike air cargo demand, previously discussed institutions rarely

publish data on the air cargo supply side. IATA publishes air cargo

supply data in its annual World Air Cargo Statistics (WATS). The data is

expressed in Available Cargo Tonne Kilometres (ACTK) by reporting

airline and is divided into international and domestic ACTK, and

scheduled, charter and all cargo operations. ACTK is compared towards

CTK to determine the weight load factor. Another way of measuring air

cargo supply is by calculating the Available Cargo Tonnes (ACT). ACT

considers the available capacity of a flight regardless of the distance

of this flight. Due to the scope of this research, the ACT capacity is

preferred as the focus is on weight parameters rather than

weight-kilometre parameters.

One problem with ACT data is the need for more publicly available

data. To solve this problem, data from flight traffic websites were

collected and processed to build a comprehensive database. The

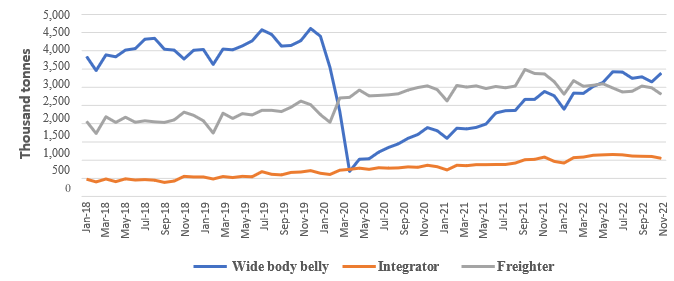

methodology can be found in section 3.2. Figure 5 illustrates the ACT on

an international level, divided into wide-body belly capacity, dedicated

freighter capacity, and integrator capacity. The data reveal that in

2019 around 59% of the capacity can be allocated to wide-body belly

capacity on international traffic. This allocation is higher compared to

the 50% market share on an industry level published by Boeing. This

would indicate that freighter and integrator capacity have a higher

domestic market share than international levels. Indeed, when domestic

data is included in the equation, the 59% wide-body capacity decreases

to a market share of 51%, relatively close to the market share published

by Boeing. The reason for the lower market share for wide-body on an

international level compared to a domestic level is twofold. First, the

data show that in 2019 54% of integrator data was dedicated to domestic

flights increasing the overall freighter capacity on the domestic

markets. Second, Anchorage is one of the world’s largest airports for

in-transit flights, connecting Asia with North America. Because

Anchorage is part of the United States, many freighter flights

connecting Anchorage with other United States airports are counted as

domestic flights.

Figure 5: International available cargo tonne evolution for

belly, integrator and freight capacity.

Figure 5 illustrates the impact of the COVID-19

pandemic on the air cargo market. Due to the travel restrictions,

wide-body belly capacity plummeted to around 700,000 ACT in April 2020.

Since 2021, wide-body passenger capacity started its slow recovery

process. In December 2022, the international wide-body belly capacity is

still 36% under 2019 levels. Freighter capacity and, to a lesser extent,

integrator capacity started increasing after March 2020 to substitute

the declining wide-body belly capacity. In 2022, freighter and

integrator capacity accounted for 57% of international ACT. Although the

current methodology provides us with some interesting data, it has three

main areas for improvement. First, the narrow-body freighter and

narrow-body passenger aircraft should be included in Figure 5. Although narrow-body aircraft

generally operate on domestic routes in larger countries like the United

States or Australia, in Europe and certain parts of Asia, narrow-body

aircraft operate cross-border flights. Second, preighter aircraft data

is currently included as wide-body belly capacity. Although preighter

flights did not occur in 2018 and 2019, IATA and Boeing’s data show a

10% market share of preighter aircraft in 2020, with peaks up to a

market share of 25% in May 2020. As of 2022, preighter flights accounted

for a market share of 5%. Last, the aircraft payload data used in the

current methodology is based on maximum payload figures. The maximum

payload is seldom reached as multiple factors, like flight distance,

airport elevation, jet stream, etc., can influence the payload. Using a

maximum payload, the data and results are subject to overestimation.

Indeed, when dividing the international cargo tonnes carried by the

international available cargo tonnes for the 2019 data, a load factor of

48.8% was found. This load factor is lower than the 50.4% indicated by

IATA, indicating an overestimation of the international ACT as demand

data for both calculations is the same.

4.3 Combining Demand and supply on

an international level

The above two components, demand and supply, were discussed

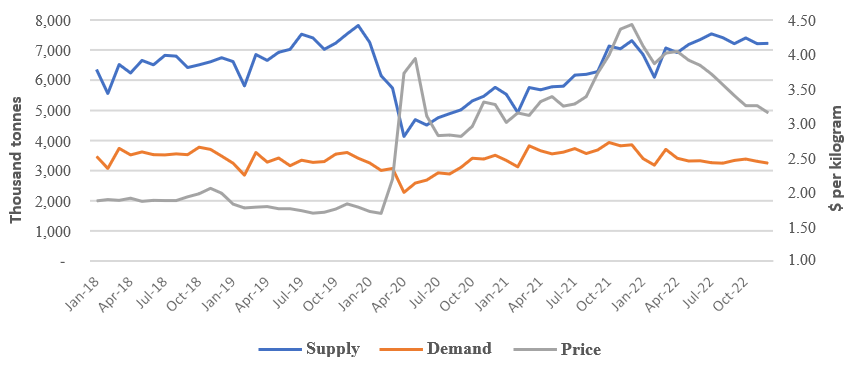

separately. Figure 6 shows those components combined with

air cargo rates provided by the World_ACD from January 2018 until

December 2022. Both demand and supply are expressed in cargo tonnes,

including double counting due to transfers, while the air cargo rates

are expressed in a price per kilogram chargeable weight. In 2019, the

international air cargo demand decreased by around 5% compared to 2018.

Due to the air passenger growth in the first two years, wide- body belly

capacity increased. Next to the wide-body belly capacity, the freighter

and integrator capacity also expanded on the international market.

Despite the decrease in air cargo demand, the increase of freighters and

integrators on an international level can be explained due to the

decline in domestic demand, making international routes more profitable

than domestic routes. The same happened in the following years, where

the freighter and integrator share on the international routes increased

while it decreased on the domestic routes. The increased supply and

decreased demand caused air cargo rates to decline on an international

level between January 2018 and December 2019. Since the outbreak of the

COVID-19 Pandemic, air cargo supply has plummeted due to the grounding

of wide-body belly capacity.

Over the last three years, the air cargo supply almost recovered to

pre-COVID-19 levels. As Figure 5 illustrates,

supply recovery is more due to additional freighter and integrator

capacity in the market than the wide-body belly capacity recovery.

Although the COVID-19 pandemic impacted air cargo demand, the impact was

relatively small, and the demand recovered quickly, reaching a

record-breaking year in 2021. The Ukraine-Russian war and the subsequent

economic recession caused air cargo demand to decrease in 2022. After

air cargo rates almost tripled in April 2020, they declined to double

the pre-COVID-19 rate around the summer of 2020 nearly. Between the

summer of 2020 and 2021, air cargo rates stabilised as demand and supply

increased. In the last three months of 2021, air cargo rates increased

from around $3.2 per kilogram to around $4.4 per kilogram. As air cargo

supply increased significantly more than air cargo demand, air cargo

rates were expected to decrease. The reason they grew rather than fell

can be found in the supply chain issues on the pacific trade lines,

where demand increased, and supply could not keep up. This problem

resulted in rates of above $15 per kilogram on some routes. Because of

the significant size of those trade lines, the exceptionally high rates

can also be found in the international air cargo rate data, which is a

weighted average of the individual market trade lines. Since the start

of 2022, air cargo rates have decreased to around $3.2 per kilogram at

the end of 2022.

Figure 6: An air cargo supply, demand and price evolution

from January 2018 until December 2022.

5 Disaggregated main trade line

market analysis

This section will discuss air cargo market imbalances between eleven

pre-defined regions. The imbalances are both estimated and discussed for

the demand and supply sides. The demand imbalances are estimated based

on sales tonnes rather than actually carried tonnes. This way, transfer

and in-transit data are excluded revealing the actual origins and final

destinations of air cargo flows. The supply imbalances are estimated for

the three types of supply: wide-body belly, freighter, and integrator

capacity. Afterwards, both the demand and supply imbalances are

compared.

5.1 Air cargo demand imbalances on

a region-to-region level

Regarding air cargo demand imbalances, Boeing provides carried tonnes

data between regions in their bi-annual world air cargo forecasts. IATA

provides CTK data in its IATA WATS or its online published reports. Both

data types have been discussed by the institutions (Boeing, 2022) and in

the literature (Morrell and Klein, 2019). Air cargo sales tonnes between

regions have yet to be analysed and discussed. The benefit of studying

air cargo sales tonnes is that it does not include double counting due

to transfers. It shows the first origin of the cargo and its final

destination. By excluding double counting, one can better analyse

whether a region is an importing, exporting or balanced air cargo

region. Double counting may blur the image and hides the actual cargo

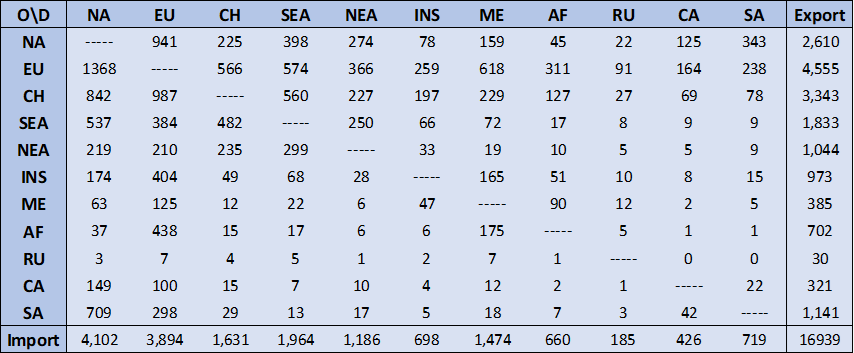

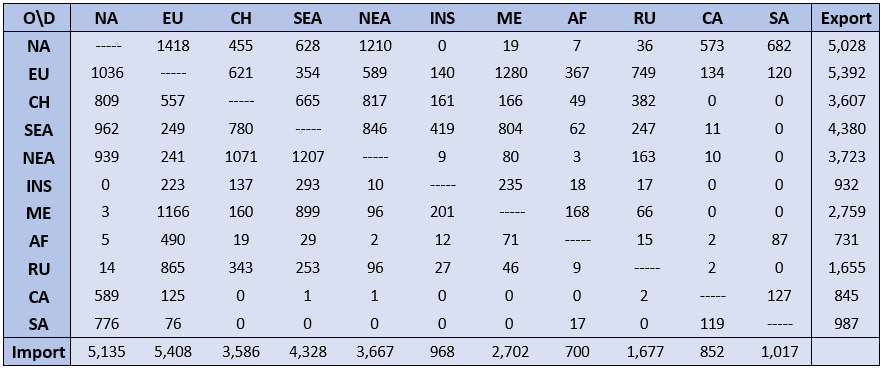

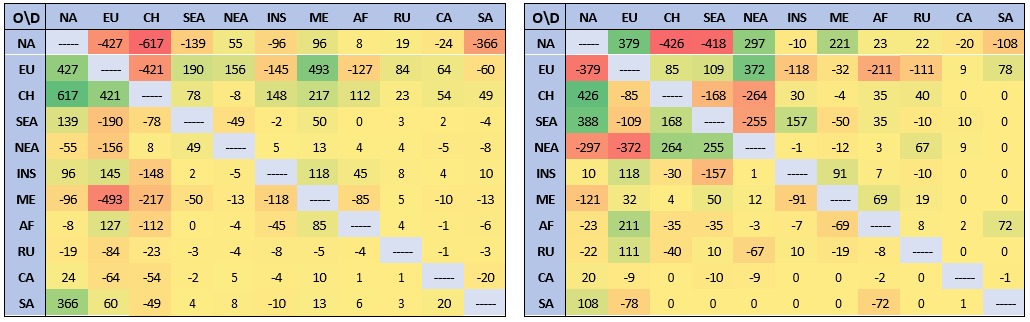

flows. For example, as Figure 7 indicates,

78,000 tonnes of air cargo originating in China and finding their final

destination in South America were sold in 2022. This 78,000 tonnes of

cargo is enough to fill 780 B777F flights with maximum payload,

indicating the significance of this route. When looking at actual

carried tonnes, traffic between China and South America is not found as

the flight distance is too far.

Figure 7 provides a matrix of the eleven

defined regions and the sales tonnes of cargo sold in 2022 between those

regions; the importance of the Northern Hemisphere trade lines can be

seen. The most extensive air cargo trade lines are between Europe and

North America, followed by China to Europe and China to North America.

The fifth biggest trade line, South America to North America, may be

surprising. This trade line is characterised by perishable cargo, mainly

fruit and vegetables. Europe is the leading exporting region, with an

export of 4.56 million tonnes of export cargo. North America is the most

extensive importing region, with 4.10 million tonnes of imported cargo.

China is a typical export market as its export is more than double its

import. China is a production country importing raw materials by sea

trade and exporting intermediate or finished products. On the other

side, the Middle East can be considered an importing region with an

import of 1.47 million tonnes compared to its export of 0.39 million

tonnes.

Overview of sales tonnes transported between the studied

regions in 2022 (thousand tons).

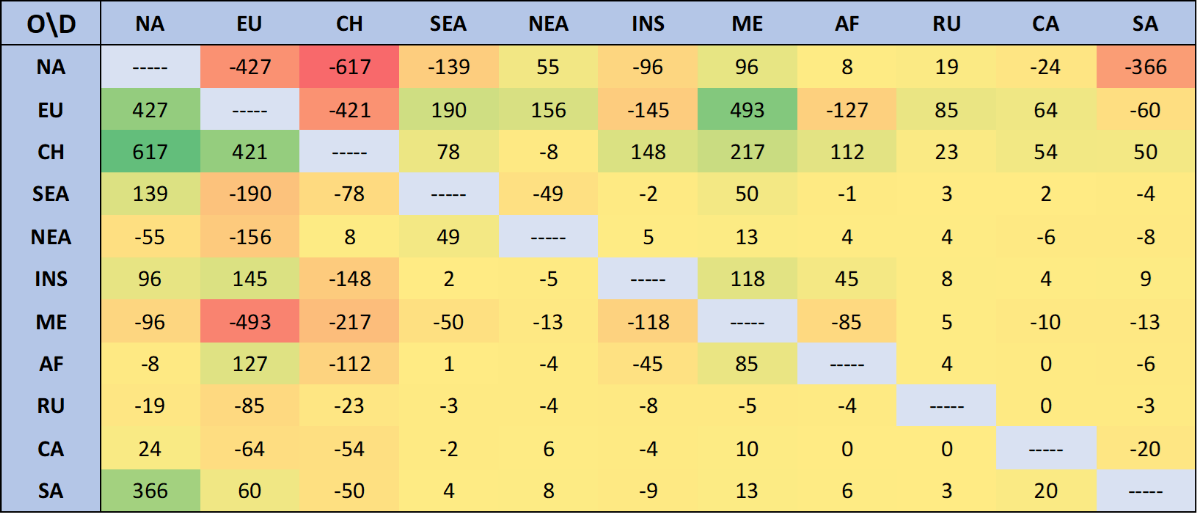

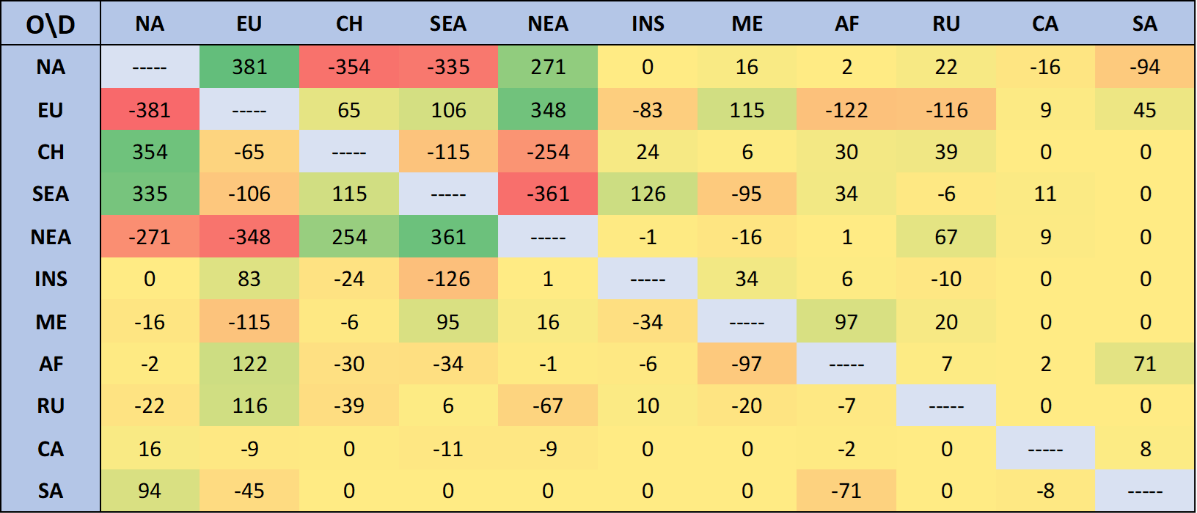

Regarding trade imbalances, Figure 8 gives an

overview of the imbalances in absolute terms between the different

regions. Around half of the trade lines are imbalanced markets with an

imbalance larger than 50,000 tonnes. The region pair with the most

significant imbalance is the China - North America route, with an

imbalance of 617,000 tonnes. China’s export to North America is 617,000

tonnes higher than its import from North America. Other highly

imbalanced routes are Europe – North America, Europe – Middle East,

China – Europe, and South America – North America Routes. The total

imbalance between export and import does not have to be the same for all

its exporting and importing regions. Europe, for example, has a positive

trade weight balance with North America, meaning that Europe’s air

export volumes to North America are higher than its import volumes.

While Europe has a positive trade weight balance with the Middle East,

Southeast Asia, and Northeast Asia, it has a negative trade weight

balance with China, the Indian Sub-Continent, and Africa. Another region

with both positive and negative trade weight balances is the Indian

Sub-Continent which has a positive trade weight imbalance with Europe,

North America, and the Middle East but a negative trade imbalance with

China. Generally, most regions are characterised by either a negative or

a positive trade weight imbalance. For example, China has a positive

trade imbalance for almost all its routes, while the Middle East and

North America have a negative trade imbalance.

Overview of the sales tonnes imbalances between the studied

regions in 2022 (thousand tons).

5.2 Air cargo supply imbalances on

a region-to-region level

5.2.1 Air cargo supply imbalances

for the freighter network

Air cargo supply imbalances have been studied by Bombelli et al.

(2020), who analysed the air cargo supply network. They mainly focused

on origin-destination pairs on an airport-to-airport level. The main

contribution of the next section will be the allocation between

freighter, integrators and wide-body belly capacity, and on the

region-to-region rather than the airport-to-airport approach. The data

used in this section is from 2022 and was collected from flight tracking

websites. It includes both wide-body passenger and freighter aircraft

and narrow- body freighter aircraft. Further information on the

methodology can be found in Section 3.

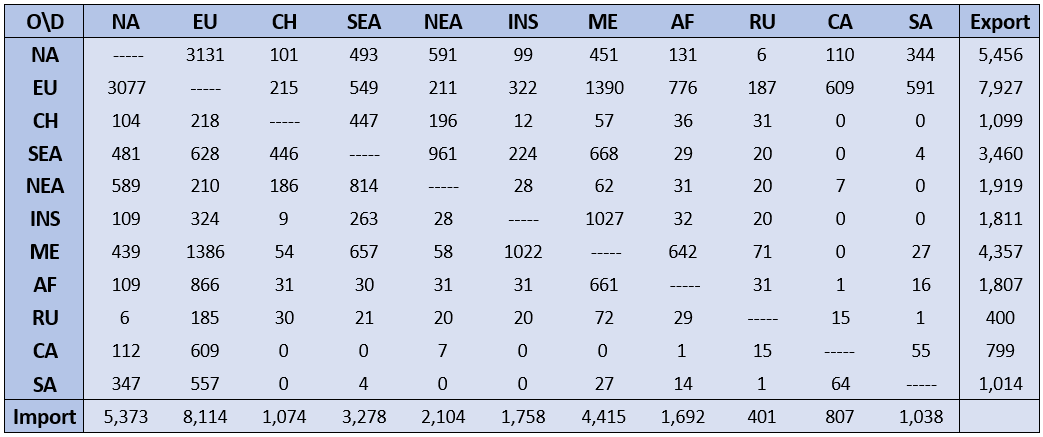

The freighter network is the most imbalanced one of the three studied

types. Figure 9 gives an overview of the ACT between

the studied regions. Compared to the air cargo demand, air cargo supply

inbound has to be equal or almost equal to outbound. This is not the

case for air cargo demand, as the load factor of the aircraft is

different on different trade lines. As Figure 9 indicates,

there is some variation between the inbound and outbound capacity of the

same region. The data assumes the maximum payload of each aircraft type

without considering other factors like flight distance, weather

conditions, airport elevation, etc., which can impact the payload. The

reason for those imperfections can be found in the data of the flight

tracking website themselves and the incompleteness of specific data

points causing flights to be deleted in the cleaning process. Routes

with a high freighter capacity are generally considered routes with a

low wide-body belly capacity or a high air cargo demand. As for air

cargo demand data, freighter aircraft data shows that air cargo is

mainly a Northern Hemisphere business.

Overview of the freighter capacity between the studied

regions in 2022 (thousand tons).

Figure 10 illustrates the freighter imbalances

between different regions. The biggest imbalances are between North

America – Europe, Southeast Asia – North America, China – North America,

Europe – Northeast Asia, and Northeast Asia – Southeast Asia. Those

imbalances are generally between the main three air cargo regions;

Europe, North America and Asia. As is not the case for air cargo demand,

those imbalanced regions cancel each other out as inbound aircraft

capacity should be the same as outbound capacity. Figure 11 illustrates the imbalances which are

higher than 50,000 tonnes. Some potential triangular or multisector

flight sectors can be found based on those imbalances. The main

potential sectors are CN-NA-NEA-CN, NEA-RU-EU-NEA, EU-ME-AF-EU,

EU-ME-AF-SA-NA-EU, SEA-INS- EU-SEA, and EU-CN-NA-EU as can be seen on

Figure7. In-depth database analysis is needed to identify the actual

sectors’ flow and how often they are operated.

Overview of the freighter capacity imbalances between the

studied regions in 2022 (thousand tons). Overview of the top 20 most imbalanced routes based on

freighter capacity in 2022.

5.2.2 Air cargo supply imbalances

for the integrator network

The integrator capacity is generally less imbalanced than the

freighter capacity but more imbalanced than the wide-body belly

capacity. Integrator traffic is even more northern hemisphere focused

than its freighter counterpart. When observing Figure 12, one might notice a 100,000 tonnes

imbalance between Southeast Asia’s outbound and inbound capacity.

Although general gaps are explained due to cleaning, data provision, and

processing errors, a 100,000 gap on an average-size route is

exceptional. A more in-depth database analysis is required to understand

better what type of error causes a gap of around 7.5% in the data.

When it comes to imbalances, Figure 12 indicates

an unusual imbalance between North America and the Middle East. No

records were found for flights from the Middle East to North America.

This is unsurprising as the Middle East is generally an import region,

importing high- end products from developed regions like North America.

The same imbalance can be found between Southeast Asia and the Middle

East and between the Indian Sub-Continent and the Middle East. From the

Middle East, the excess capacity flies to Europe to be redistributed to

North America or Southeast Asia. Another significant imbalance exists

between North America and China/Southeast Asia. This imbalance also

occurred on the freighter network. At the same time, the imbalance

between North America and Northeast Asia is more minor but also in the

other direction, from North America to Northeast Asia.

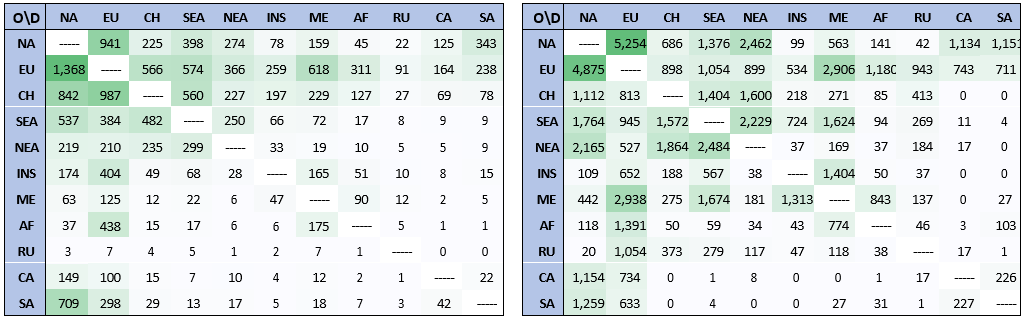

Overview of the integrator capacity between the studied

regions in 2022 (thousand tons).

5.2.3 Air cargo supply imbalances

for the wide-body belly network

The air cargo wide-body belly capacity is generally balanced between

the trade lines. Although aircraft generally operate both legs of an

origin-destination pair, this is not always the case. Sometimes airlines

perform one leg with an A350-900 aircraft and the other with a B777-

300ER. Both aircraft have another air cargo belly-hold payload causing

inconsistencies in the data. The reason airlines often switch aircraft

on both legs of the same route can be twofold. First, on a long-haul

flight, due to the jet stream, the flight time on one leg can be up to

two hours longer than the flight time on the other leg. The two-hour

longer flight leg requires a higher payload for fuel resulting in a

lower payload for cargo in the belly hold. Airlines can optimise their

air cargo operations by using more cargo-friendly or more efficient

aircraft on highly cargo-imbalanced routes. Due to the imperfection and

data aggregation, it is unclear on which routes and how often those

switches happen. Further research into the database is needed to analyse

how often a different aircraft is used on one leg compared to the return

leg. Also, more research on the reason behind those switches is needed.

Although it is difficult to say which routes are imbalanced due to those

aircraft switches, two region-to-region combinations stand out. First,

the Europe to Southeast Asia route has an ACT of 549,000 tonnes, while

the Southeast Asia to Europe route has a payload of 628,000 tonnes.

Second, the Europe to Africa route has a payload of 776,000 tonnes

compared to the 866,000 tonnes on Africa to Europe route.

Overview of the wide-body belly capacity between the

studied regions in 2022 (thousand tons).

5.3 Comparison of air cargo supply

and demand imbalances

As discussed above, both air cargo demand and supply are imbalanced

between regions. Comparing sales tonnes demand imbalances with available

cargo tonnes imbalances is useful for two reasons. First, while a

region’s total inbound and outbound are not equal for air cargo demand,

they should be similar for air cargo supply. Aircraft entering a region

either keep flying in the region or leave the region, meaning that their

inbound and outbound capacity should be equal considering the usage of

the aircraft’s maximum cargo payload. The difference between inbound and

outbound may cause disparities in the market. Second, by observing the

sales tonnes rather than the carried tonnes, transfer data and double

counting are excluded from the comparison. By excluding the transfer

data, it is possible to get an indication of the transfer and in-transit

region on a global market. Although the comparison may give a valuable

indication, more research is needed on integrator express data as it is

excluded from the demand side but included in the supply side.

Currently, there is no publicly available information on how much cargo

and express integrators carry and between which markets. Furthermore,

more in-depth research is needed to estimate how many transfers are

taking place and where they are happening. This requires a significant

amount of detailed data, which is, to our best knowledge, yet to become

available for academic research. Based on the sales tonnes data we

received and the capacity database we built, we derived which regions

are transfer or in transit regions. However, it will be challenging due

to the above-described reasons.

Figure 14 compares the total sales tonnes and

total available capacity between regions for 2022. Based on this

comparison, some interesting aspects can be found. First, the Russian

and Central Asia region has low import and export tonnes but high ACT.

Transits can explain the high supply flows but low demand flows. Many

airlines land at airports in Central Asian countries to refuel, as jet

fuel is relatively cheap. The four main countries where aircraft might

refuel are Azerbaijan, Kazakhstan, Kyrgyzstan and Uzbekistan. Those four

countries accounted for 32% of the inbound originating from and outbound

to Europe, East Asia and China in 2019. Those three regions are the

three main regions flying to and from Central Asia. The 32% represents

around 615,000 ACT and might seem small as it only accounts for